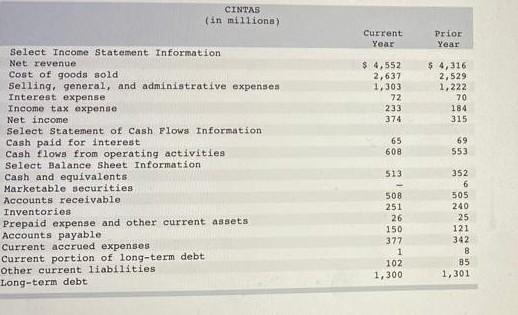

According to tha data,

Receivable stock Turnover ratio = Credit sales / Average debtor

= $4,552 / ($505+$508)÷2

= $4,552 / $506.5

= 8.99

Inventory stock Turnover ratio = Cost ot goods sold / Average Inventory

= $2,637 / ($251+$240)÷2

= $2,637 / $245.5

= 10.74

Current ratio = Current assets / current liabilities

Current assets=$513+$508+$251+$26 = $1,298

Current Liabilities = $150+$377+$1+$102 =$630

Current ratio = $1,298 / $630

= 2.06

Cash ratio = Cash and cash equivalents / Total current liabilities

= $513 / $630

=0.81

Tines Interest earned ratio = Earnings before interest and tax (EBIT)/ Interest

EBIT = Net income + Tax expense + Interest expenses

= $374 + $233 +$72

= $679

Times interest earned ratio = $679 / $72

= 9.43

Cash Coverage ratio = Cash flows from operating activities / Cash paid for interest

= $608 / $65

= 9.35

Learn more about stock here:

brainly.com/question/25818989

#SPJ4

The formula for finding the net present value is -C0 + [C1 / (1 + r)] + [C1 / (1 + r)²] + [C1 / (1 + r)³].

<h3>What is the net present value?</h3>

The net present value is a capital budgeting method. Net present value is the present value of after-tax cash flows from an investment less the amount invested.

Only projects with a positive net present value should be accepted. A project with a negative net present value should not be chosen because it isn't profitable. When choosing between positive net present value projects, choose the project with the highest net present value first because it is the most profitable.

An advantage of the net present value method of capital budgeting is that it considers the times value of money. A disadvantage of net present value is that it is difficult to estimate the accurate discount rate.

To learn more about net present value, please check: brainly.com/question/25748668

#SPJ1

Answer:

Compute the decrease in net income that the company should anticipate in the off season

Net income decrease in $2475

Explanation:

contribution margin=price-associate cost

55%=100%-45%

Revenue 4500 100%

Cost 2025 45%

Contribution margin 2475 55%

Answer:

- $ 138,000

Explanation:

The investment activities includes the transaction done on purchasing the equipment and selling the land.

Thus, for the given question

The list of investment activities:

Purchase of Equipment = - $ 149,000

Proceeds from Sales = $ 130,000

Purchase of Land = - $ 119,000

here, the negative sign depicts the amount is paid

thus, the net cash flow from the investment activities

= - $ 149,000 + $ 130,000 + (- $ 119,000)

or

the net cash flow from the investment activities = - $ 138,000