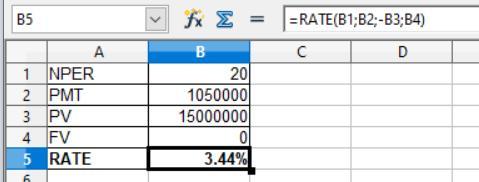

Answer:

3.44%

Explanation:

For this question we use the RATE formula that is shown on the attachment

Data provided in the question

Present value = $15,000,000

Future value or Face value = $0

PMT = $1,050,000

NPER = 20 years

The formula is shown below:

= Rate(NPER;PMT;-PV;FV;type)

The present value come in negative

So, after solving this, the rate pf the return is 3.44%

Answer:

a1. 60 days

a2.Remittance = $40,500

b1- 1 % discount offered

b-2, 10days

b-3 =$40,095 ± 0.1

c-1 Implicit interest $405 ± 0.1%

c-2 Days' credit days=50 days

Explanation:

a1. 60 days

a2.0rder for 300 units of inventory at a unit price of $135

Remittance = 300($135)

Remittance = $40,500

b- 1 % discount offered

b-2, 10days

b-3 Remittance (1- 0.01) $40,500

(0.99)$40,500

Remittance =$40,095 ± 0.1%

c-1 Implicit interest $40,500- $40,095

Implicit interest $405 ± 0.1%

c-2

Days' credit days 60-10

Days' credit days=50 days

Answer:

Mark-up = 50%

Explanation:

Given the following data;

Selling price = 15 Pesos

Purchasing cost = 10 Pesos

To find the mark-up;

First of all, we would determine the profit;

Profit = 15 - 10

Profit = 5 Pesos

Now, we can solve for the mark-up using the formula below;

Mark-up = 50%

Earnings per share is "$2.5".

We can calculate this in such a way;

<span>Earnings per share = After-tax income or earnings /number of shares outstanding

</span>= <span>$375,000 / $150,000

= $2.5</span>