Answer:

For Part 1, 3 and 4 Please see the attached images.

For Part 2 Please see the solution below.

Explanation:

Part - 1:

Please see the attached picture.

Part - 2:

August 3rd:

Debit: Cash $1,200

Credit: Accounts Receivable $1,200

To record collection of cash from debtors.

August 5:

Debit: Cash $1,300

Credit: Common Stock $1,300

To record receiving cash from issuing common stocks.

August 6:

Debit: Accounts Payable $2,700

Credit: Cash $2,700

To record payment to creditors.

August 7:

Debit: Cash $3,000

Debit: Accounts Receivable $3,500

Credit: Services $6,500

To record earnings from services on cash and on accounts.

August 12:

Debit: Equipment $1,200

Credit: Cash $400

Credit: Accounts Payable $800

To record purchase of equipment on cash and on accounts.

August 14:

Debit: Salaries Expense $3,500

Credit: Cash $3,500

To record payment of salaries.

Debit: Rent Expense $900

Credit: Cash $900

To record payment of Rent.

Debit: Advertising expense $275

Credit: Cash $275

To record payment of advertising expenses.

August 18:

Debit: Cash $3,500

Credit: Accounts Receivable $3,500

To record cash collection from debtors.

August 20:

Debit: Dividends Payable $500

Credit: Cash $500

To record payment of dividends payable.

August 24:

Debit: Accounts Receivable $1,000

Credit: Services $1,000

To record services performed on accounts.

August 26:

Debit: Cash $2000

Credit: Accounts Payable $2,000

To record note payable from Laurentian Bank within 6 months.

August 27:

No Transaction needed. If the prepayment has been made by client then then transaction would have been recorded. But neither Payment is received in advance nor services have been performed in advance, So no transaction needs to be recorded at this moment.

August 28:

Debit: Utilities Expense $275

Credit: Accounts Payable $275

To record utilities expense occurred and due in September.

August 31: paid income tax for the month of $500.

Debit: Income Tax $500

Credit: Cash $500

To record payment of Income Tax.

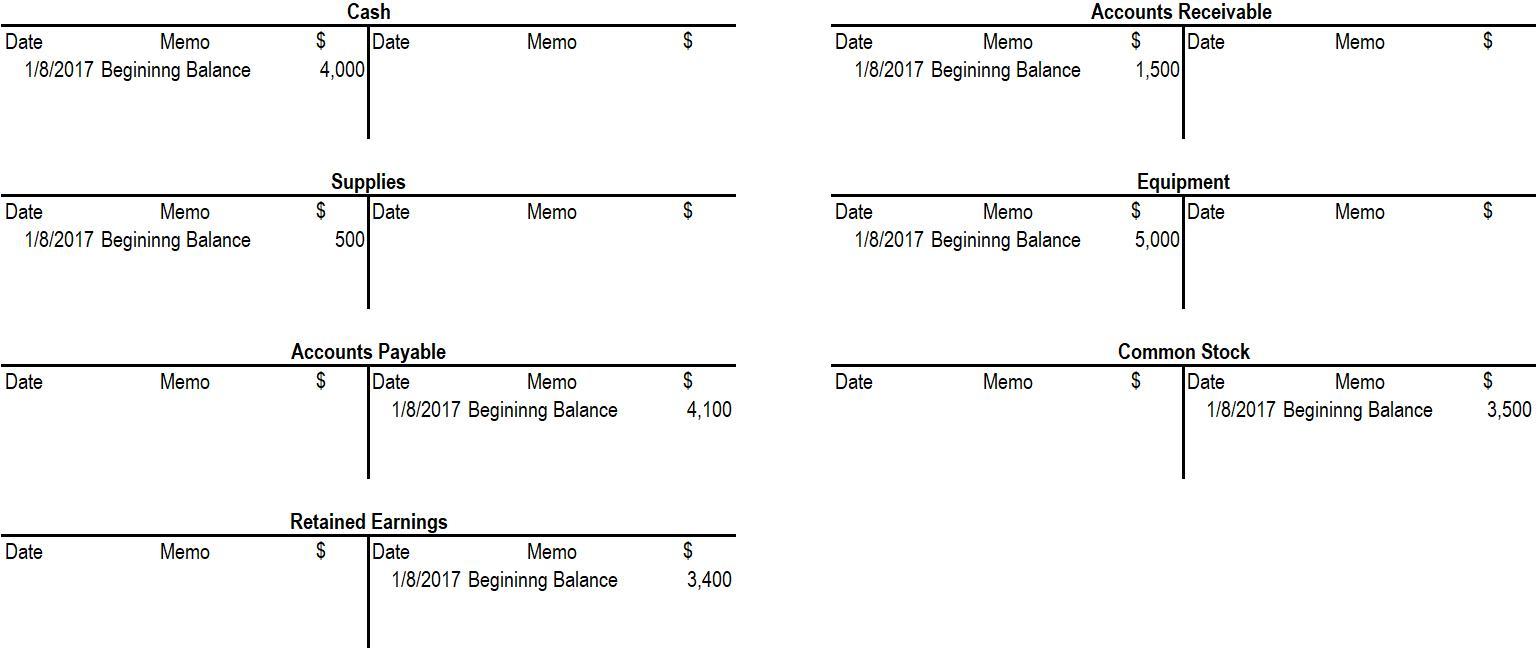

Part 3:

Please see the attached Picture.

Part 4:

Please see the attached Picture.