Answer:

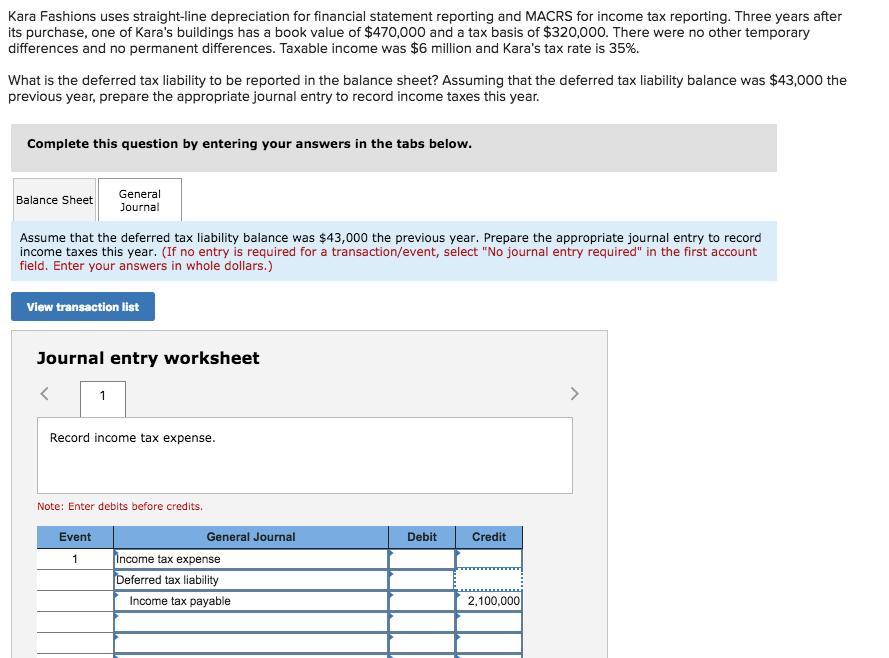

Income Tax Expense a/c Dr $ 20,57,000

Deferred Tax Liability a/c Dr $ 43,000

To Income Tax Payable a/c Cr $ 21,00,000

($6 Million x 35%)

Explanation:

The Above will result in timing Difference.

Timing Differences are those which can be reversed in subsequent periods.

Income Tax Expense a/c Dr $ 20,57,000

Deferred Tax Liability a/c Dr $ 43,000

To Income Tax Payable a/c Cr $ 21,00,000

($6 Million x 35%)

( Being Entry Passed for Tax Expense and Timing Difference Adjusted through Deferred Tax Liabilty)