Answer: The unit Product cost is $32.09

Explanation:

$

Add : Direct Material. 35

Add: Direct Labour 16

-------------

Prime Cost. 51

Add: variable manufacturing overhead. 15

Add: Fixed manufacturing overhead. 24,000

-----------------

Production cost. 24,066

-------------------

To determine the unit Product cost for the year we will divide the production cost by the unit produced

Production cost ÷ unit produced

Since the the production cost is $24,066 and unit produced is 750unit

24,066÷ 750

= 32.088

= 32.09

Therefore the unit Product cost is $32.09

Answer:

A. A shipping employee who performs the same lifting motion over and over.

Explanation:

Answer:

Yes, a large percentage of consumers are influenced by people who are present on the internet, who are mostly younger people. In order to generate income, advertisements for young people are becoming less and less advertising look like.

For this reason, advertising pieces should always aim to entertain and inform, only to later sell. The experience with advertising content should be positive.

The teen audience may have many different tastes, but there is a high probability that everyone will use a cell phone. The device is part of the daily lives of young people and it is through it that teenagers communicate, consume content, and even shop.

Answer:

Franchising

Explanation:

Franchising is defined as the contract that exists between a parent company (franchisor) and other firms (franchisee) in which an operating licence is given to the franchisee.

The franchisor gives access to use of their brand and also provides support and training to the franchisee.

Franchisee in turn gives an agreed amount of profit to the franchisor for using their brand.

An established name and specific rules of operation is agreed upon in the contract.

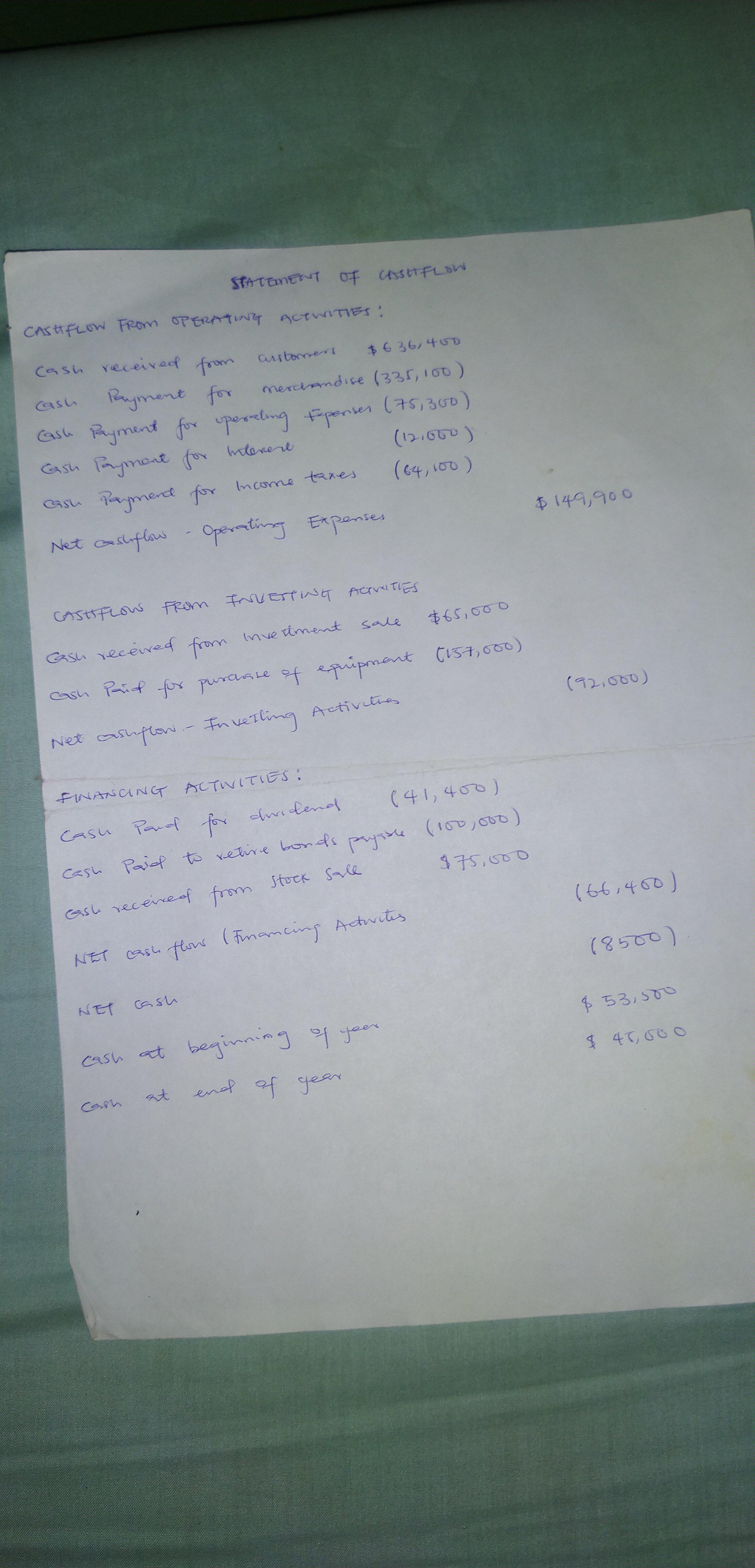

Answer:

Kindly check attached picture

Explanation:

Kindly check attached picture for detailed statement using the direct method