Answer:

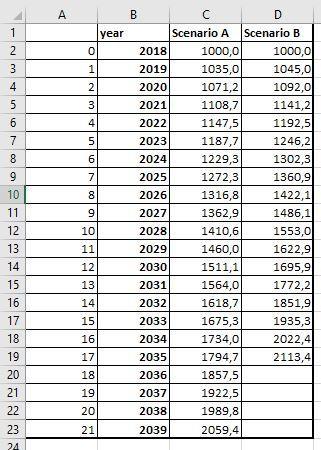

2. 20 years under scenario A, versus 16 years under scenario B

Explanation:

It is clearer if I explained with an example:

Let suppose that a nation´s real GDP for 2018 was 1000. In scenario A you will have:

2019:1000*3.5%=1035

2020:1035*3.5%=1071,2

and so on, the same for scenario B

2019: 1000*4,5%= 1045

2020: 1045*4,5%= 1092

and so on.

I attached an excel table where you can see that: in the first scenario, between year 20 and 21 (2038 and 2039) the GDP will double and in the second one, between year 15 and 16 GDP will double. The answer is 2.

Large companies and corporations usually have this kind of method. Company abc gave a common stock<em> </em><em>(also known as common stock) </em>to each and every stockholder in the company. It represents ownership in a corporation. Stock holders are also given the right to vote and chose among themselves the board of directors.

Answer:

$120,669

Explanation:

Ending Retained Earnings = Opening Retained Earning + Net Income - Dividends

therefore,

Ending Retained Earnings = $90,369 + $46,300 - $16,000 = $120,669

thus,

Ending balance in Retained Earnings be next year will be $120,669

A antonym for delicate could be firm