Answer:

Lower of $2,400

Explanation:

In this question, we have to compare the total fixed manufacturing cost between the two methods which are shown below:

On January 1

= Number of units × fixed manufacturing cost

= 6,000 units × $3

= $18,000

On December 31

= Number of units × fixed manufacturing cost

= 5,200 units × $3

= $15,600

The difference between these two amounts would be $2,400 ($18,000 - $15,600)

In the variable costing, this cost should not be recognized in the income statement while in absorption costing, this cost should be recognized in the income statement as it is goes to the cost of goods sold as an expense.. So, the net income lower of $2,400

Answer:

C. $26,689.46

Explanation:

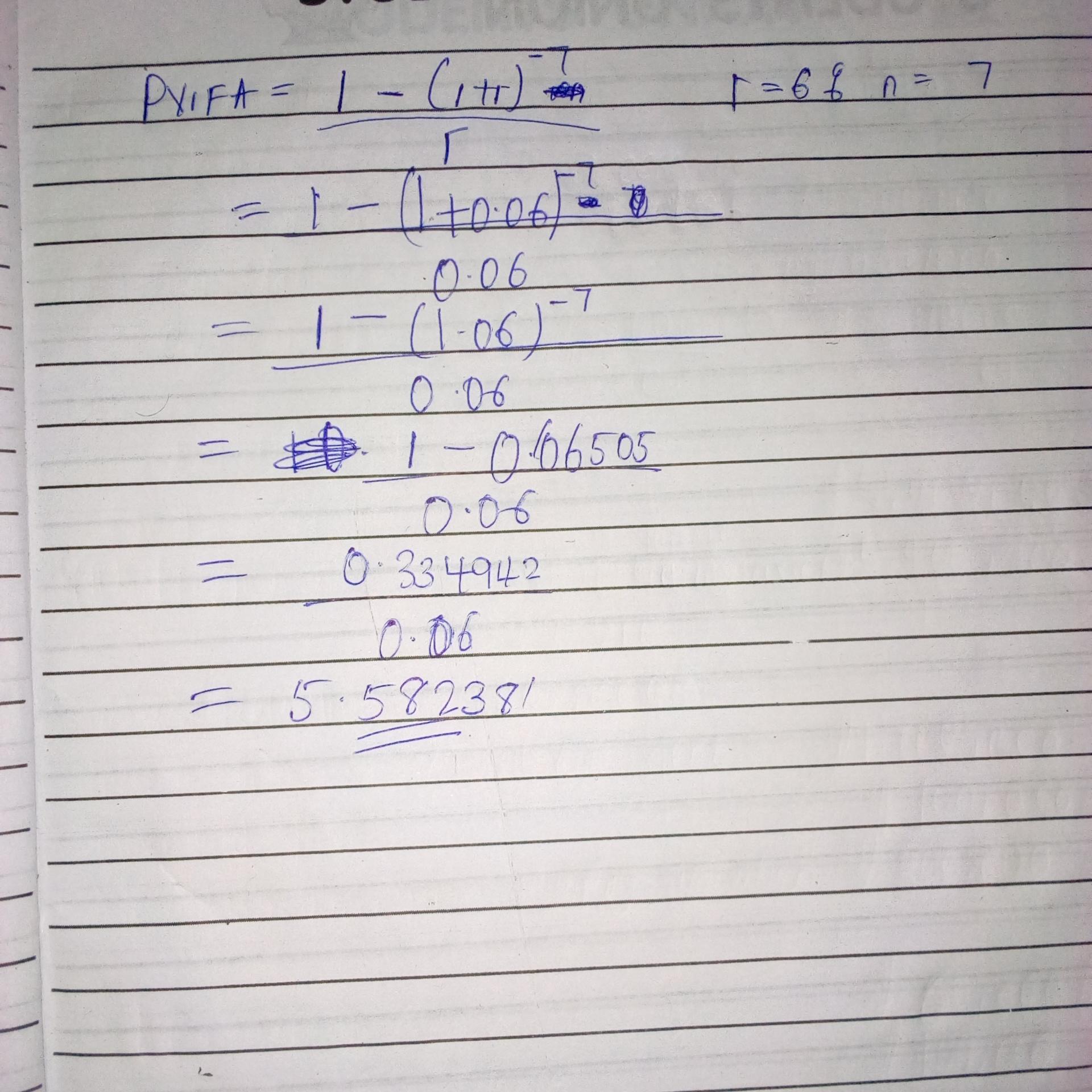

Computation of the present value is

Annual payment × (PVIFA of 7 years, 6%)

Where PVIFA = (1-(1+r)^-n)/r

Where n= Number of period

r= Rate applied

PVIFA = 5.5824 (Kindly check attached picture for explanation

= $4,781 × 5.5824

=$26,689.46

Answer:

<em>The</em><em> </em><em>corr</em><em>ect</em><em> </em><em>answe</em><em>r</em><em> </em><em>is</em><em> </em><em>:</em><em>-</em> Measurable gain

Answer:

Use the same estimations and computations as accounts receivable to determine cash realizable value.

Explanation:

Notes receivable is a balance sheet item, that records the value of promissory notes that a business is owed and has the right receive payment for.

Short term notes receivable are due within a period of one year from the balance sheet date and are catergorised under current assets in the balance sheet.