Answer:

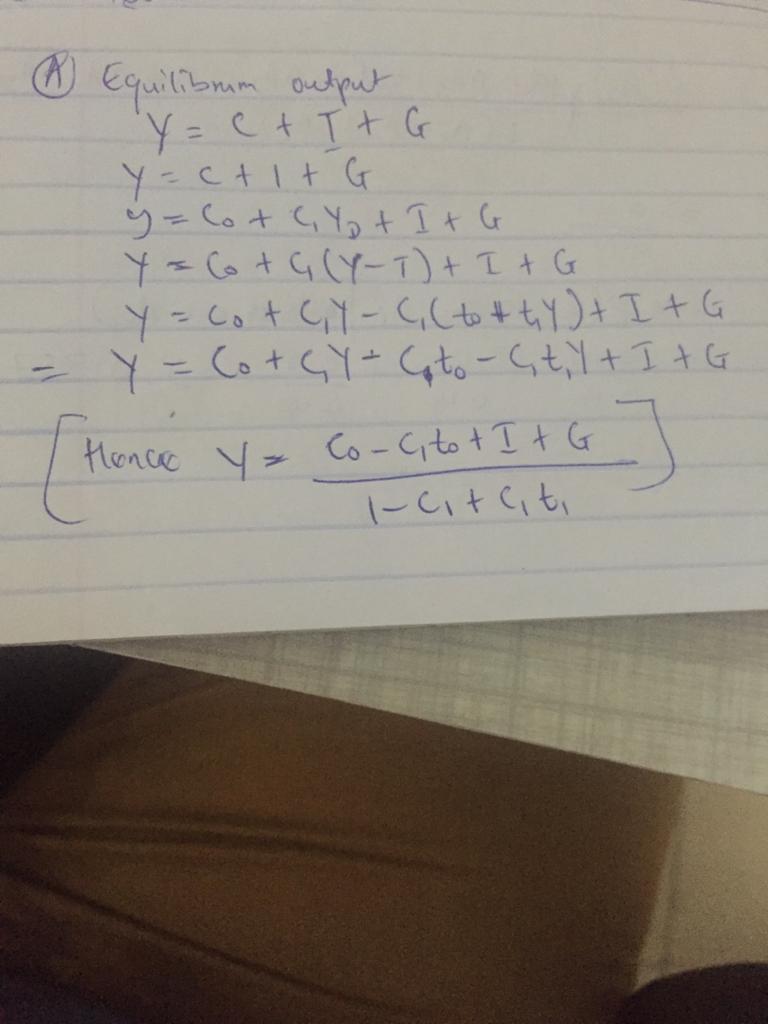

A) attached below

B)

C) The fiscal policy is called an automatic stabilizer because the taxes are dependent on the level of income and also the output of the multiplier is more stable because it doesn't respond to rapid changes in fiscal policies.

Explanation:

Given data:

C = Co + C1YD

T = t0 + t1Y

YD = Y - T

G and I are both constant

C1 lies between 0 and 1 while T1 lies between 0 and 1

A ) solving for equilibrum output

attached below

B) The multiplier

Multiplier =

The economy responds to changes in autonomous spending when t1 is 0 but responds less when t1 is positive, this is because the more positive t1 is the lower the multiplier value

c) The fiscal policy is called an automatic stabilizer because the taxes are dependent on the level of income and also the output of the multiplier is more stable because it doesn't respond to rapid changes in fiscal policies.

Arts Direction

that is the answer

hope it works

Answer:

A market economy answers the three economic questions by allocating resources and goods through markets, where prices are generated.

There are two extremes of how these questions get answered. In command economies, decisions about both allocation of resources and allocation of production and consumption are decided by the government. In market economies, there is private ownership of resources—established though property rights—and the factors of production and consumption are all coordinated through markets. In a market system, resources are allocated to their most productive use through prices that are determined in markets. These prices act as a signal for buyers and sellers. Most economies are mixed economies that lie between these two extremes.

In either system, a rational agent would allocate resources and production using marginal analysis. In command economies, this is more difficult to do because without markets, prices fail at being an effective signal.

Explanation:

I hope this helps!!

Answer:

6.08%

Explanation:

Rosita's restaurant has a sales of $4,500

The total debt is $1,300

The total equity is $2,400

The profit margin is 5%

=5/100

= 0.05

Therefore the return on assets can be calculated as follows

= profit margin×sales/total debt +total equity

= 0.05×$4,500/($1,300+$4,200)

= 225/3,700

= 0.0608×100

= 6.08%

Hence the return on assets is 6.08%

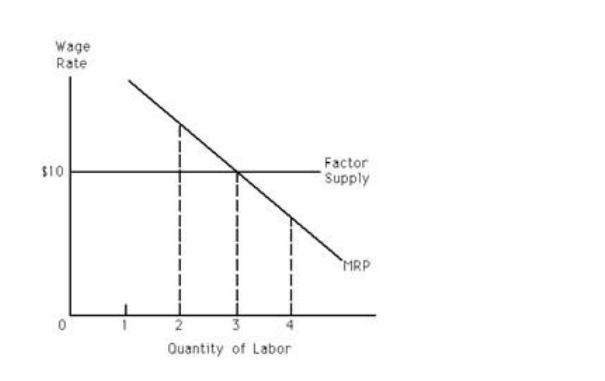

Answer:

d) it can hire all the workers it wants to at the going wage rate.

Explanation:

The price taker means the company or an individual is ready to accept the prices that are prevailed in the market

In the case when a firm is a price taker in the labor market also it cannot set the prices as expected. The attached diagram represent the flat supply curve. It hire the workers depend upon the MPR and the factor supply curves

Therefore in the given situation, the last option is correct