<span>Office of Management and Budget examines the cost of a bill. A proposed bill is given a cost forecast, and they conduct in-depth analysis while also ensuring the bill is legal. The Office of Management and Budget is also responsible for budget proposals.</span>

In the new long-run equilibrium, there would be an increase in the number of suppliers of t-shirts.

<h3>What would happen when the demand for plan white t-shirts increase?</h3>

A perfect competition is when there are many buyers and sellers of homogenous goods and services. Market prices are set by the forces of demand and supply.

When demand for t-shirts increase, there would be an excess of demand over supply. This would lead to a shortage. This would increase the price of t-shirts. In the long run, more suppliers would enter into the industry and this would increase supply of t-shirts. As a result, equilibrium would be restored.

To learn more about perfect competition, please check: brainly.com/question/17110476

#SPJ1

Answer:

• The employee’s privacy is an important consideration and payroll workers need to be aware of updated information as it becomes available.

• The Privacy Act of 1974 allows an employee access to their payroll records.

• Review U.S. Department of Labor OCFO-1 or the U.S. Department of Health and Human Services Privacy Act 09-40-0006

Explanation:

The options are:

• Employees of publicly owned companies may have access to each other’s payroll records.

• The employee’s privacy is an important consideration and payroll workers need to be aware of updated information as it becomes available.

• The Privacy Act of 1974 allows an employee access to their payroll records.

• Review U.S. Department of Labor OCFO-1 or the U.S. Department of Health and Human Services Privacy Act 09-40-0006.

The advice that I would give her about privacy laws and payroll are that the privacy of the employee’s is vital and that the payroll workers should always be aware of information that are updated whenever they're available.

Also, the Privacy Act of 1974 allows an employee to be able to access their payroll records. Lastly, they must review U.S. Department of Labor OCFO-1.

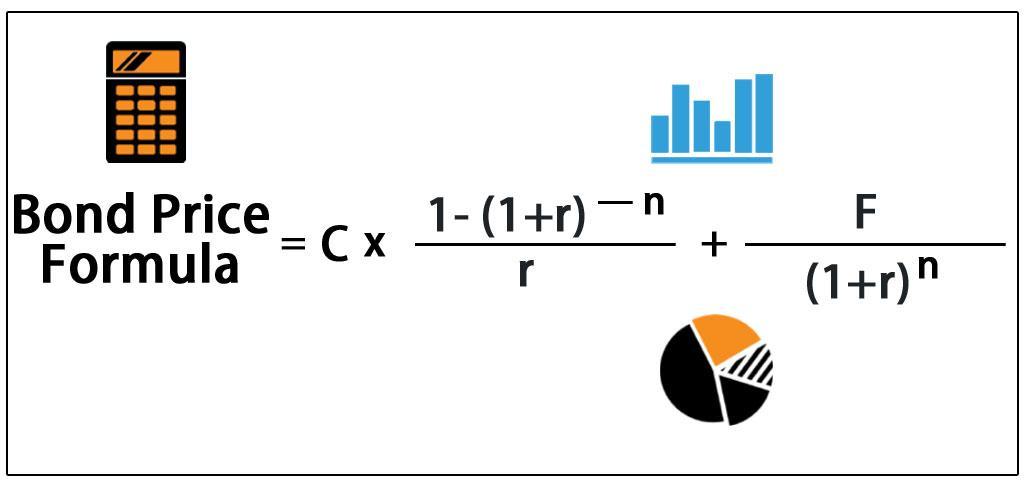

Answer:

Bond Price = $945.2631228 rounded off to $945.26

Explanation:

To calculate the price of the bond today, we will use the formula for the price of the bond. We assume that the interest rate provided is stated in annual terms. As the bond is an annual bond, the coupon payment, number of periods and annual YTM will be,

Coupon Payment (C) = 1000 * 0.0675 = $67.5

Total periods (n) = 30

r or YTM = 0.072 or 7.2%

The formula to calculate the price of the bonds today is attached.

Bond Price = 67.5 * [( 1 - (1+0.072)^-30) / 0.072] + 1000 / (1+0.072)^30

Bond Price = $945.2631228 rounded off to $945.26

<span>Assets = liabilities + owners' equity is the equation for information reported on the: Balance sheet

In accounting, balance basically represents a brief overview about what the company currently own.

Assets represent something valuable that the company own to conduct their operation, Liabilities represent the debt that they have to pay to other individual or entities, And owner equity represents how much ownership one person have from all the things that the company owns.</span>