Answer:

b. 9.00%

Explanation:

For the computation of WACC first we need to follow some steps which is shown below:-

Step 1

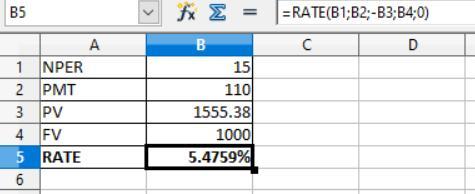

Cost of debt = 5.48% which is explained with the help of attachment.

Given that,

Present value = $1,555.38

Future value or Face value = $1,000

PMT = 1,000 × 11% = $110

NPER = 15 years

The formula is shown below:

= Rate(NPER;PMT;-PV;FV;type)

The present value come in negative

So, after applying the above formula, the cost of debt is

Step 2

Cost of preferred stock = Annual preferred dividend ÷ Price

= $8 × $92.25

= 0.086721

Step 3

Cost of equity = Dividend ÷ (Stock price × (1 - flotation cost)) + Growth rate

= 2.78 ÷ (33.35 × (1 - 0.08)) + 0.092

= 18.26%

WACC = Weight of debt × Cost debt) + (Weight of preference stock × Cost of preference stock) + (Weight of equity × cost of equity)

= (0.58 × (0.0548 × (1 - 0.4)) + (0.06 × 0.086721) + (0.36 × 0.1826068)

= 9.00%