Complete Question:

Yasmin Company expects to sell 1,900 units of finished product in January and 2,250 units in February. The company has 270 units on hand on 1st January and desires to have an ending inventory equal to 20% of the next month's sales. March sales are expected to be 2,350 units. Prepare Yasmin's production budget for January and February.

Answer:

680 Units for January and 250 units for February.

Explanation:

Production Budget can be calculated using the following formula:

<u>Production Budget = Expected Sales + Desired Ending Inventory Units - Opening Inventory</u>

The formula is reflected in a tabular form below:

<u>Production Budget For Yasmin Incorporation</u>

January February

Expected Future Sales (Unit) 900 250

<u>Add:</u> Desired Ending Inventory Units 50 70

<u>Less:</u> Openning Inventory Units <u> 270 </u> <u> 70 </u>

Production Units 680 250

Answer:

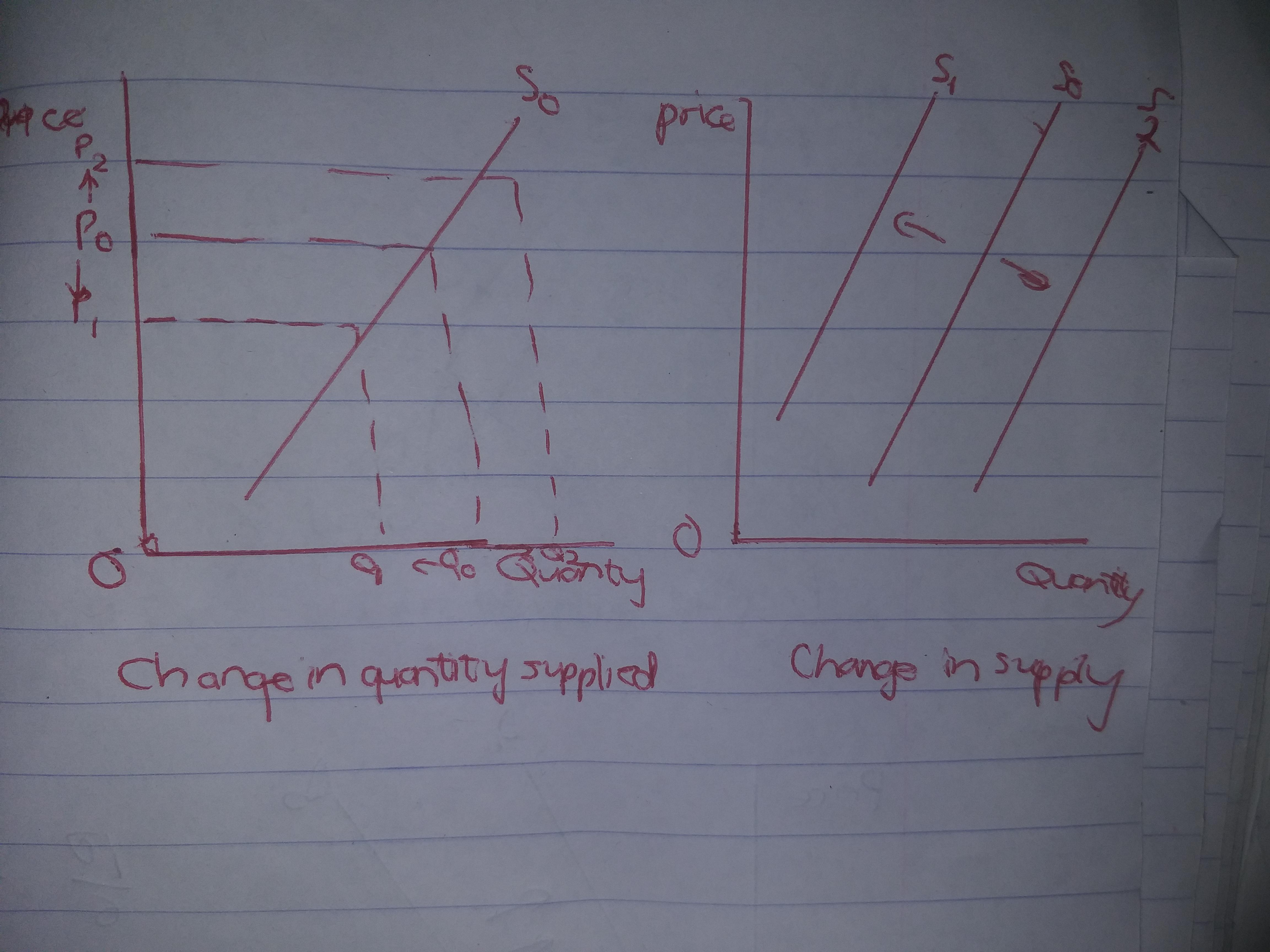

b. supply is represented graphically by a curve and quantity supplied as a point on that curve.

Explanation:

Qunatity supplied shows how qunatity of a product changes in response to changes in price of that good. According to the law of supply, the higher the price of good, the higher the quantity supplied and the lower the price of a good, the lower the quantity supplied. This shows that quantity supplied has a direct relationship with price.

Changes in quantity supplied is shown by movement along a supply curve.

Changes in supply is caused by other factors other than changes in price. Some of these factors are :

Changes in price of similar goods

Tax

Change in number of suppliers

Technological advancement

Changes in supply is shown by movement of the supply curve either to the left or to the right and not a movement along the supply curve.

I hope my answer helps you

Churches .it's a religious institution

Answer:

C)

Explanation:

He can file a strict liability lawsuit against Big Ben Forts for failure to provide adequate instructions on assembling the product.

Answer:

5.38% and 5.1%

Explanation:

In this question, we are asked to calculate the after tax return to the corporation and the after tax return to the investor.

What is meant by after tax return is simply the profit made after we subtract the amount of taxes. It is simply revenue less the amount of tax paid.

We calculate the values as follows:

For the corporation;

The after tax return can be calculated by the following mathematical expression;

After tax return to Corporation = 0.06 - (0.06 * 0.3) * 0.34 = 0.0538 = 5.38/100 which is same as 5.38%.

After tax return to the individual investor = 0.06(1-0.15) = 0.06 * 0.85 = 0.051 or just 5.1%