Answer:

Aftermarketing

Explanation:

Aftermarket IMG is defined as the set of activities a business undertakes after making a product sale to retain customers and to foster repeat sales.

For example following up on the customer to ascertain level of satisfaction with the purchase, after sale technical support, and complaint management.

In the given scenario ID Groups Corp maintains a database that contains customer information and a history of each of their purchases, offers ongoing guidance on product maintenance, and responds quickly to complaints and seeks customer satisfaction.

These are aftermarketing activities.

Answer:

moot

Explanation:

If a case is settled prior to trial for any cash, we say that the lawsuit is now subject to debate, and it is commonly known as moot. In several law schools across the globe, students are taught how to deal with moot. However, it is not very easy to give a ruling concerning moot, this is because there is little or no practical evidence. It is at sometimes referred to as moot court.

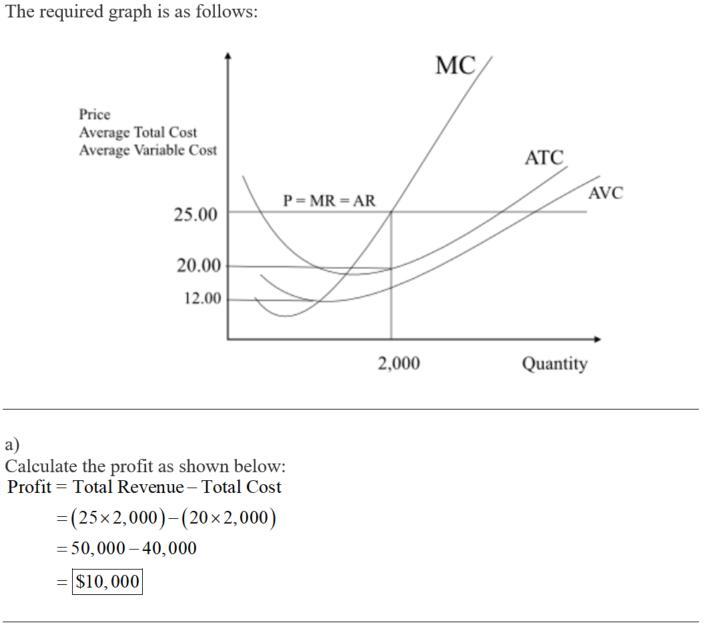

Answer:

a) $10,000

b) $12

c) The grower has a loss at the shutdown price

d) New firms will enter the market in the long run

Explanation:

Find the given attachments

Answer:

direct channel (or producer to consumer)

Explanation:

This channel is appropriate when a producer is trying to introduce an innovative product or service and wants to reach a large audience. The best way a manufacturer or producer can sell its products or services directly to consumer is through internet sales.

Answer:

Explanation:

A. Accounts Receivable - Number of sales invoices

B. Central Purchasing - Number of purchase requisitions

C. Computer Support - Number of computers

D. Conferences - Number of conference attendees

E. Employee Travel - Number of travel claims

F. Payroll Accounting - Number of payroll checks

G. Telecommunications - Number of cell phone minutes used

H. Training - Number of employees trained.