Answer:

Aids to trade communication

<u><em>Aids to trade includes Transport, Communication, Warehousing, Banking, Insurance, Advertising, Salesmanship, Mercantile agents.</em></u>

Trade promotion organizations in a country and Global organizations for international trade. These important auxiliaries ensure a smooth flow of goods from producers to the consumers.

Hope this helpssss :)

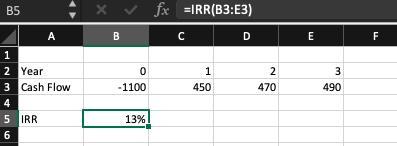

Answer:

13%

Explanation:

To solve for the IRR we first need the formula

where NPV is the net present value,  is the cash flow in period t, and r is the IRR (internal rate of return)

is the cash flow in period t, and r is the IRR (internal rate of return)

Solving this polynomial can be quite cumbersome. Thankfully excel has a built in function that we can take advantage of call IRR

As shown in the screen shot we write the cash flow, with the first one with the negative sign. Then we call the IRR function selecting the cells with our Cash Flow values and excel will return the IRR. In this case is 13%

Answer:

UberEATS is on a mission to make eating well effortless for everyone, everywhere. Our service connects customers to Uber-speed delivery from restaurants in over 80 cities around the world. We give people more options when choosing how to eat. We help restaurants reach more customers and build their businesses.

Answer:

Year _______Risk Premium (%)

2011 _______ 0.95

2012_______ 16.01

2013_______ 32.99

2014_______ 12.66

2015_______ 0.46

Explanation:

The Risk premium is the premium paid to an investor for investing in a risky stock/security/asset over the risk-free rate in the market.

A Risk-free rate is a rate that is offered by a security having minimum or no risk at all e.g. Rate on Government securities are considered as the risk-free rate because these securities are backed by the government.

T bills or Treasury bills are also considered as risk-free investments.

Use following formula to calculate the Risk premium

Ris premium = Stock Market Return - T-Bill Return

Use above formula Calculate the risk premium as below

Year _ Stock Market Return (%) __T-Bill Return (%)__ Risk Premium (%)

2011 _______ 0.98 _______________0.03 _________ 0.95

2012_______ 16.06_______________0.05 _________ 16.01

2013_______ 33.06_______________0.07 _________ 32.99

2014_______ 12.71 _______________ 0.05 _________ 12.66

2015_______ 0.67 _______________ 0.21 __________ 0.46

Answer:

$252,000

Explanation:

Calculation to determine How much of these salaries are common fixed expenses

Office administrative assistant $ 54,000

Office administrative assistant $39,000

President's salary $159,000

Common fixed expenses $ 252,000

($54,000+$39,000+$159,000)

Therefore How much of these salaries are common fixed expenses will be $252,000