Answer:

a. A pure strategy Nash equilibrium of a game is a strategy profile in which both players are best responding to each other's strategies. For the given payoffs, we have 2 pure strategy Nash equilibrium (June, August) and (August. June). The arguments are as follows:

- Universal playing June and Fox playing August is equilibrium. This is because given that Universal in releasing in June. FOX maximizes its payoff by releasing in August and the same reasoning applies for Universal as well.

• Universal playing August and Fox playing June is equilibrium. This is because given that Universal is releasing in August, Fox maximizes its payoff by releasing in June and the same reasoning applies for universal as well.

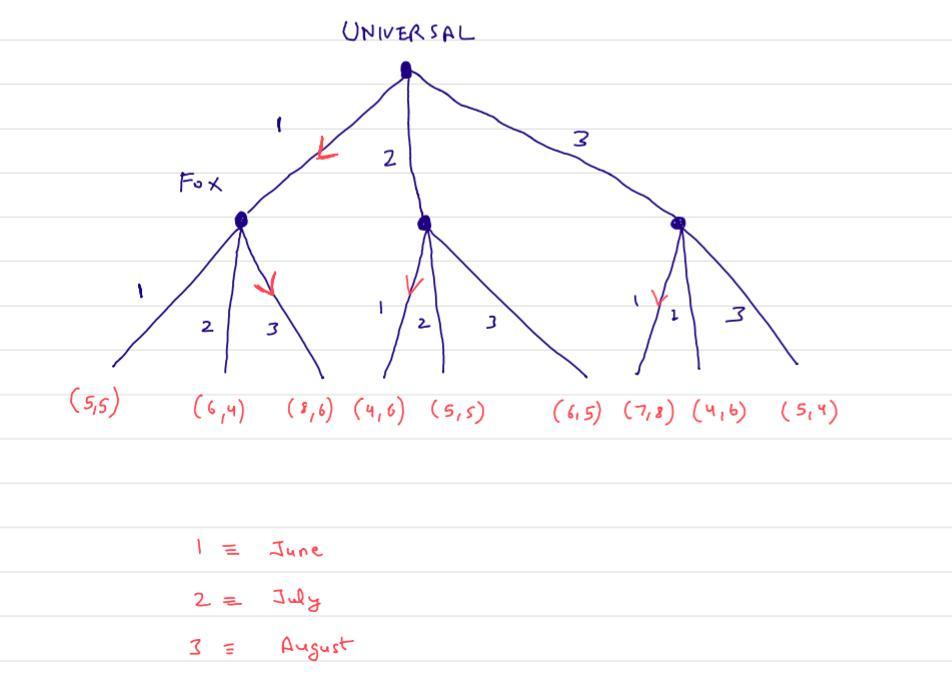

b. The extensive form diagram is given below. The sub game perfect equilibrium is computed by backward induction. Fox chooses its action given what universal has decided. These actions are marked by the red arrows. Universal therefore faces the following payoffs:

- By playing June, Universal gets 8 and Fox gets 6

- By playing July, Universal gets 4 and Foxs gets 6

- By playing August, Universal gets 7 and Fox gets *

Thus, given the above information by backward induction, Universal will choose to release in June and then Fox will release in August leading to payoffs (8,6).

Universal would want this to happen because the subgame perfect equilibrium gets rid of the Nash equilibrium that generated lower payof for them. That is , the only SPE is giving payoffs (8,6) and (7,8). Since Universal prefers 8 over 7, it would want the game to be sequential