Answer:

A. -many substitute

Explanation:

Deadweight loss is inefficiency that occurs as a result of taxation. It's the change in production or consumption as a result of tax.

If tax is imposed on a good with many substitutes, the deadweight loss would be greater because consumers can easily shift consumption to another good that is cheaper.

If a good has inelastic supply or demand, the deadweight loss is less because consumers and producers do not change quantity demanded and supplied if prices increase as a result of tax.

I hope my answer helps you.

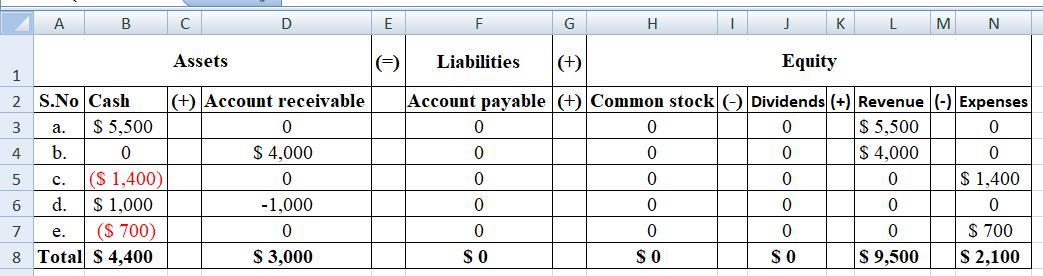

- The impact of the following transactions should be shown on the accounting equation below:

- The accounting equation comprises equity, liabilities, and assets.

- In this, the sum of the stockholder equity and the liabilities should be equivalent to the total assets.

- It analyzed the financial position, performance of the company.

Therefore we can conclude that the attachment i.e. attached represent the impact of the given transactions on the accounting equation.

Learn more about the accounting equation here: brainly.com/question/14689492

In accounting, the long-term liabilities<span> are shown on the right wing of the balance-sheet representing the sources of funds, which are generally bounded in form of capital assets. Examples of </span>long-term liabilities<span> are debentures, mortgage loans and other bank loans.

Welcome :)</span>

Answer:

The Journal entries are as follows:

(i) On January 1, 2017

Plant Assets A/c Dr. $600,000

To cash $600,000

[To record the depot]

(ii) On January 1, 2017

Plant Assets A/c Dr. $41,879

To To Asset retirement obligation $41,879

[To record the Asset retirement obligation]

Missing information: Based on an effective-interest rate of 6%, the present value of the asset retirement obligation on January 1, 2017, is $41,879.

Answer:

(A) Tangibles

Explanation:

Based on what Ryan is trying to accomplish, which is getting his customers to renew the lawn care service each year. He needs to demonstrate tangibles. Showing the customers that his service is done correctly, that it is neat and perfectly cut. Once the customers see that the job is done correctly and by professional personnel they will be more inclined on renewing the service.

I hope this answered your question. If you have any more questions feel free to ask away at Brainly.