Answer:

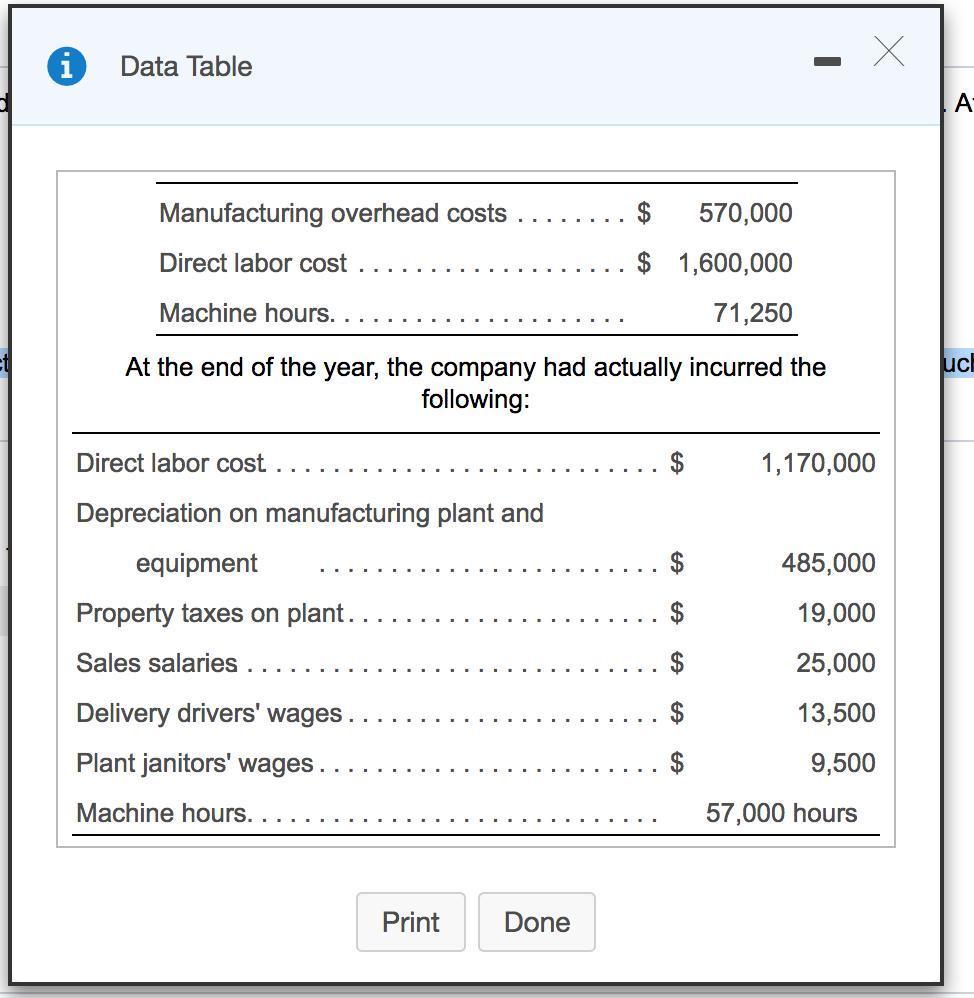

hello your question lacks the required data attached is the required data

answer : A) $513500,

B) manufacturing overhead is under allocated by $57500

Explanation:

A) How much Manufacturing overhead was incurred during the year

= depreciation on manufacturing plants and equipment + property taxes on plant + plant janitors wages

= $485000 + $19000 + $9500 = $513500

B) Is manufacturing overhead under allocated or over allocated

to check if it is over allocated or under allocated we use this formula

= actual overheads - allocated overhead

= $513500 - $456000 = $57500

therefore manufacturing overhead is under allocated by $57500

Answer:

A,B,D,E are cost which should NOT be expensed when incurred. While C is a cost which should BE expensed when incurred.

Explanation:

(a) $13,000 paid to rearrange and reinstall machinery. select an option. NO

(b) $200,000 paid for addition to building. select an option. NO

(c) $200 paid for tune-up and oil change on delivery truck. select an option. YES

(d) $7,000 paid to replace a wooden floor with a concrete floor. select an option. NO

(e) $2,000 paid for a major overhaul on a truck, which extends the useful life. NO

Therefore A,B,D,E are cost which should NOT be expensed when incurred. While C is a cost which should BE expensed when incurred.

Answer:

A. Market price

dan

c. bid price

Explanation:

I hope you

i'm sorry ya kalo jawaban nya salah

Answer:

;l'l;';l/

Explanation:l;';l'l;'

fdgbfv bhj,/..,iuxklmn jk

Answer:

Please find the complete solution in the attached file.

Explanation: