Answer:

The present value of the savings is $22222.22

Explanation:

A perpetuity is an indefinite series of equal payments made after equal intervals of time and for an unlimited period. A growing perpetuity is a kind of perpetuity whose period payments are not equal and they grow(or decline) at a constant rate each period for an indefinite period of time.

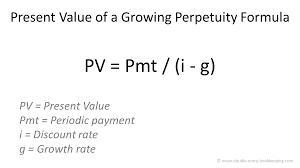

The formula for the present value of a growing perpetuity is attached.

The present value of the savings can be calculated as follows,

Present value = 2000 / (0.05 - (-0.04)

Present value = 2000 / (0.05 + 0.04)

Present value = 2000 / 0.09

Present value = $22222.22

Answer: Which of the following statements about capitalism and socialism is correct? All of the responses are correct.

Explanation: Socialist nations are less economically productive. Capitalist nations have greater economic inequality. Capitalist nations are more economically productive. All of these statements regarding capitalism and socialism are true. Capitalism is an economic and political system where the trade and industry of a country are controlled by private owners for profit instead of the state having control. Socialism is an economic and political system where different organizations control production, distribution, and the exchange of goods and services.

Answer: the actual value

Explanation:

Consistent advertisement by the cell phone company has gotten Jeremy to buy a product of their's hit Jeremy got a product which the actual value does not match his expectation. It's either Jeremy expected a lot, or was offered different categories of the brand and choose the least or that the company played on him, either of the options will be what played out as Jeremy couldn't get what he had in mind when he bought the phone. These scenario plays out many times between customers and retailers or manufacturers as some of the item they do buy don't reach what they expected, some other times it could be seen that those products were exaggerated during the advertisement.

Answer:

The total cost of the departmental Work-in-Process Inventory at the end of the period = $ 8200

Explanation:

Units % of EUP

Completion D.Materials Conversion

Costs

No Of Units

Completed 1400 100 1400 1400

<u>Units In Process 400 50% 400 200 </u>

<u>Total 1800 1800 1600</u>

Ending Inventory Valuation

Working:

Direct Materials = $( 25,200/ 1800 )*400= $5600

Conversion Costs= ($ 20800/1600)*200= $2600

Total Ending Inventory Costs= $5600+$2600= $ 8200

Direct materials (1,800 at $14.00) $25,200

Direct labor 12,480

Factory overhead 8,320

Total Manufacturing Costs $ 46000

Answer: B. Backordering is not a strategy to manage service capacity.

Explanation: Service capacity is making sure that everyone involved in the business is producing the highest possible output of their services. All staff, departments and equipments should be pushing to maintain a high level of service capacity which is why hiring extra workers to make sure the job gets done is a strategy to manage service capacity. Pricing and promotion is also a strategy to manage service capacity so that the products/services are being used.