Answer:

C.51.63%

Explanation:

Gross profit percentage = Gross profit/ Net sales ×100

Gross profit $700,400

Net sales $1,356,504

Hence ;

$700,400/$1,356,504 ×100

=51.63%

Therefore the gross profit percentage is

51.63%

Here's the options that completes the question:

A. building a state-of-the-art facility to fully capture scale economies via an export strategy.

B. using export, licensing, or franchising strategies so as to minimize risk and capital investment.

C. locating buyer-related activities in all countries where it sells its product.

D. dispersing its activities among various countries in a manner that lowers costs or else helps achieve greater product differentiation and transferring competitively valuable competencies and capabilities from its domestic operations to its operations in foreign markets.

E. avoiding the use of strategies that entail coordinating its domestic strategic moves with its strategic moves in the various foreign markets that it enters.

Answer:

D. dispersing its activities among various countries in a manner that lowers costs or else helps achieve greater product differentiation and transferring competitively valuable competencies and capabilities from its domestic operations to its operations in foreign markets

Explanation:

A key condition that makes a firm achieve competitive advantage or a favourable business position is it's costs and product design.

If a firm can lower it's cost in a foreign market while also maintaining quality just as it is has done in it's domestic market then it stands a better chance of success.

For example, if a firm in the clothing line industry decides to expand its operations to a foreign market eg Africa.

A key factor in determining its success is its ability to lower its cost in the foreign market as compared to competitors, while also achieving the same quality standards of products.

Answer: coupon rate is greater than its yield to maturity

Explanation: This is because investors are interested in high yield and will not mind paying for it in other to get a higher payment from coupon.

Yes this statement is true.

Explanation:

The sale of banana will add the twice contribution in the GDP as because the price is double and the sell of every single unit in the market in comparison of apple is able to add more currency in the economy than a sell of every single unit of apple.

The higher price may affect the sale as people will move to the other alternative but how much sell of banana will take place will able to add more money in the market as compared to apple.

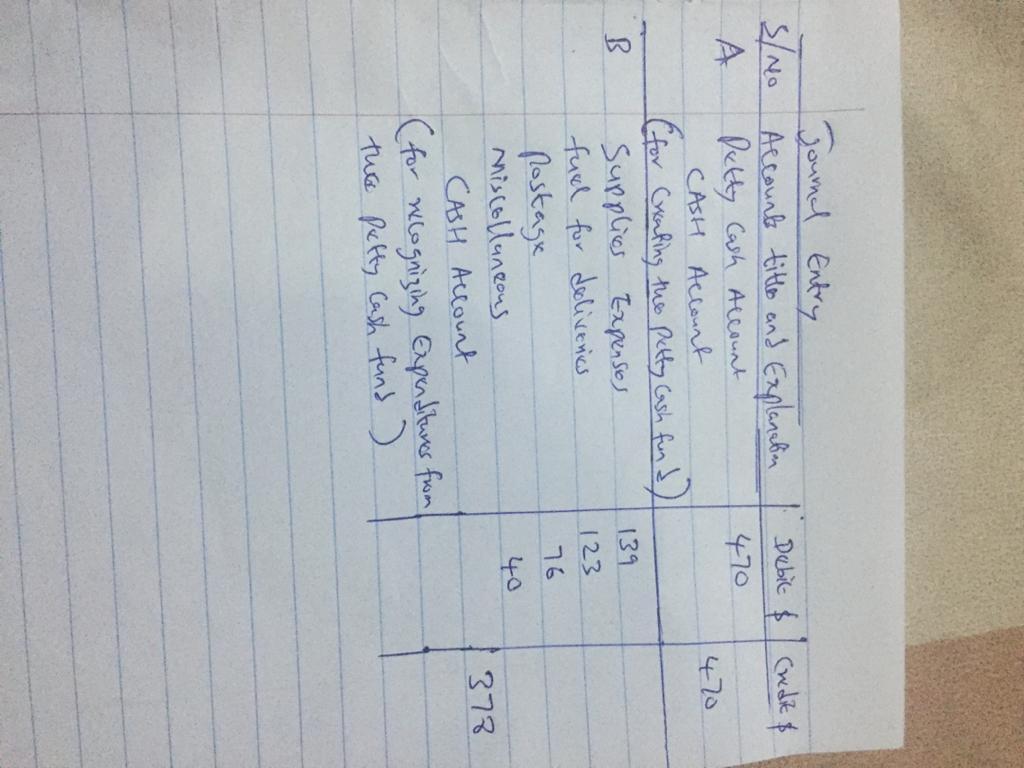

Answer:

A petty cash fund is created by debiting the petty cash account and credited to the cash account

The expenses made is debited to the respective expenses account and then credited to the cash account

Explanation:

petty cash = $470

Expenditures made by employees :

supplies = $139

Fuel for deliveries = $123

postage = $76

Miscellaneous = $40

NOTE : A petty cash fund is created by debiting the petty cash account and credited to the cash account

The expenses made is debited to the respective expenses account and then credited to the cash account

ATTACHED IS THE JOURNAL ENTRY