Answer:

Overhead= $12,420

Explanation:

Giving the following information:

Wolf Company used $5,940 of indirect raw materials and $6,480 of indirect factory labor during the period.

Factory overhead costs are the costs that can't be directly assigned to a product, service or job. This is why companies assigned overhead using manufacturing overhead rates.

In this case, the overhead is the sum if indirect material and indirect labor:

Overhead= 5,940 + 6,480= $12,420

Answer:

The lack of education and the lack of birth control.

Explanation:

1. The lack of education: The lack of education for girls is the primary reason of exceeding the population growth rate in developing countries than in developed countries. The more the educative a woman, the more the conscious that woman. Developing nations cannot afford to provide full education for their population. Moreover, many parents have the reluctance regarding the girl education that make the scenario difficult. Education promotes to a better lifestyle which encourages people to have fewer children.

2. The lack of birth control occurs due to the early marriage in developing nations. The educated people of developed nations control the birth rate as they have the knowledge of un-controlling birth rate can create problems such as food, cloths, and living places. From the discussion, it is clear that developed nations have the common sense to control the population. UN estimated that the combined population some countries is likely to be reach 1.7 billion in 2050 from 850 million.

Answer:

This manufacturer should have to take the option of dropping Dillard's and including Macy's and Saks Fifth Avenue.

Explanation:

When manufacturers produce, they do so for the sake of gains and profits. A larger market provides bigger profits compared to a smaller one.

This question tells us that this manufacturer has a greater number of customers looking to get there products at Neiman Marcus, Macy's, and Saks Fifth Avenue. So since these places would provide him a bigger market, so he should partner with these retail markets (Neiman Marcus, Macy's, and Saks Fifth Avenue) and drop the market with just few customers (dillards).

Answer:

Puffery

Explanation:

PUFFERY can be defined as the way of using exceptional words to describe things in which such things described are exaggerated or false praise for the purpose of attracting buyers to that particular product or service.

Although PUFFERY are commonly been used in advertising or to promote sales which is why PUFFERY is often not taken serious due to the fact that it is subjective.

In order word PUFFERY can said to means the way of using false praise to praise something in which such things or item are just be exaggerated just as in the case of

Melon Lawn who describe XJ200 as a "fabulous new mower" that will "take landscaping by storm in order to attract customers to the products.

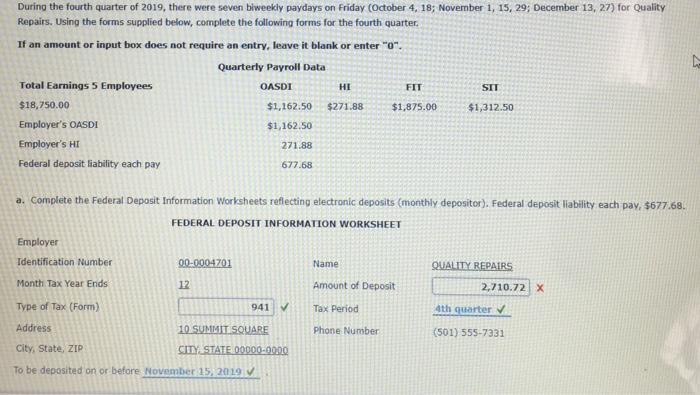

Answer:

<em>The missing figures for Worksheets are</em>;

<u>Type of Tax (Form)</u> - 941

This is used by Employers to report the taxes they withheld from Employee .

<u>Amount of Deposit</u> - $1,355.36

The Federal Deposit Liability per pay was $677,68. There was biweekly payments meaning 2 payments were made in the month so this figure must be multiplied by 2.

= 677.78 * 2

= $1,355.36

<u>Tax Period</u> - 4th Quarter (stated in question)

<u>To be deposited on or before</u> - November 15, 2019

This is because when paying monthly, the due date is always on the 15th of the following month.