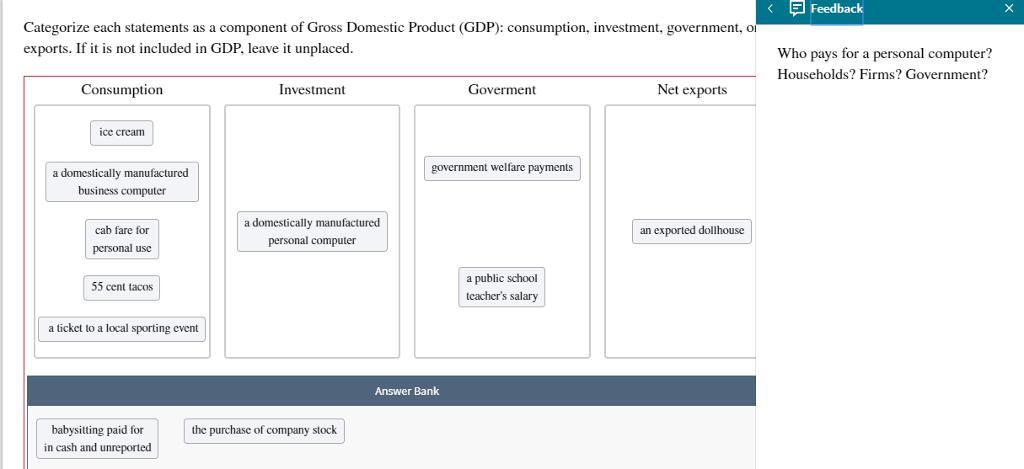

Answer:

The Gross Domestic Product (GDP) is a measure of the value of all final Goods and Services in an Economy in a given period usually a year.

It can be calculated using the Expenditure method which is;

= <em>Consumption + Investment + Government Spending + Net Exports</em>

Consumption

Here, the final goods and services that all households in the Economy purchased and used for the year are included. It is usually the largest component of GDP.

The following will fall here.

- <em>Ice cream</em>

<em>- A domestically manufactured personal computer</em>

<em>- Cab fare for personal use</em>

<em>- A ticket to a local sporting event</em>

<em>- 55 cent tacos</em>

Investment

The Goods that will fall under here include Capital goods purchased or made in an Economy for the purpose of increasing production capacity.

Of the goods listed only one will fall here being;

- <em>A Domestically Manufactured Personal Computer. </em>

<em />

Government Spending

This includes all Public Spending in the Economy on goods and services for things such as Health and Defense but excluding transfer payments such as Social Security.

- <em>Public School Teacher's Salary will fall under here. </em>

Net Exports

These are the Exported goods from the country less the goods that it imported. From the above only one item falls under this category;

- <em>Exported Doll House</em>