Answer:

Some examples of pricing objectives include maximising profits, increasing sales volume, matching competitors' prices, deterring competitors – or just pure survival. Each pricing objective requires a different price-setting strategy in order to successfully achieve your business goals

A leader cheers up the gang and makes people wanna strive hard and en-suite to be like them. It also creates loyalty which is good for business. Leaders also give clarity.

Answer:

March 31

Dr. Payroll Tax Expense: 3071.25

Cr. FICA- Social security taxes payable:

1395

Cr. FICA- Medicare taxes payable:

326.25

Cr. SUTA-State unemployment taxes payable:

1215

Cr. FUTA- Federal unemployment taxes payable: 135

Explanation:

March 31

Dr. Payroll Tax Expense: 3071.25

Cr. FICA- Social security taxes payable:

(6.2%×$2,250) 1395

Cr. FICA- Medicare taxes payable:

(1.45%×$2,250) 326.25

Cr. SUTA-State unemployment taxes payable:

(5.4$×$2,250) 1215

Cr. FUTA- Federal unemployment taxes payable: (0.6%×$2,250) 135

Answer:

Please find the complete question in the attached file.

Explanation:

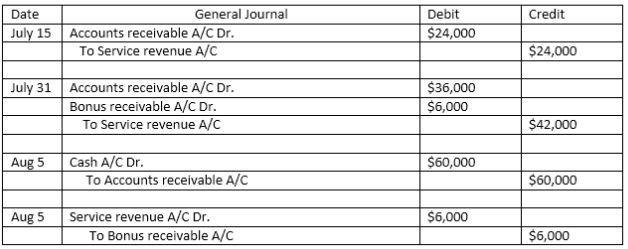

Rocky believed there would be a  possibility of a July bonus for touring, i.e

possibility of a July bonus for touring, i.e  , from July 1-July 15 (10 days)-. Therefore no bonus can be calculated as

, from July 1-July 15 (10 days)-. Therefore no bonus can be calculated as  / day trip \times 10 days = throughout this duration.

/ day trip \times 10 days = throughout this duration.

The expected 15-day revenues from 16th July – 31st July may well be calculated as  Rocky calculated that it would get the bonus

Rocky calculated that it would get the bonus  of the time. Estimates a

of the time. Estimates a

Answer:

E) 0 units of A and 200,000 units of Z.

Explanation:

In order to estimate the profit maximizing sales mix we first calculate the contribution per product per limiting factor. Limiting factor in this case is the labor hours.

So,

Contribution per hour if A is made = 8 * 12 = $96

Contribution per hour if Z is made = 10 * 10 = $100,

Therefore Z holds priority,

Since there is no sales mix we need to follow we can just make Z for maximizing profits and as such We make 20000 * 10 = 200,000 units of Z and 0 units of A.

Hope that helps.