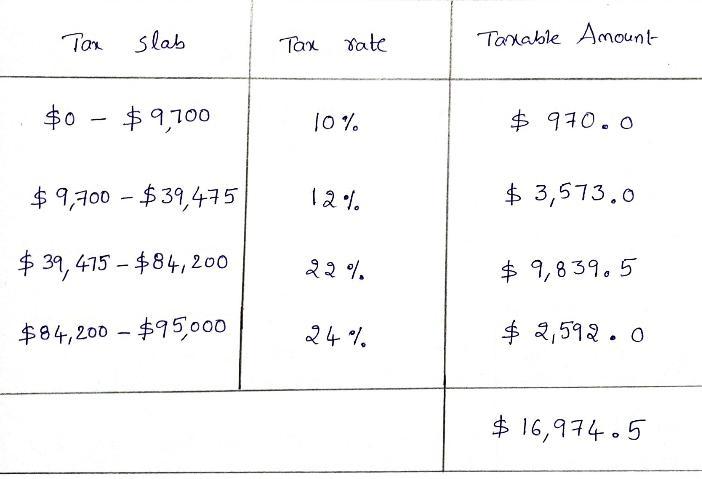

Answer:

Gross tax liability is $17,725. None of the options is correct.

Explanation:

For capital gain tax rate is 15%

-> 5.000 * 15% = 750.

Total gross tax liability is 16.974.5 + 750 = 17.725

The amount 16.974 is calculated based on the table attached in this answer.

Answer:

18%

Explanation:

The computation of the average rate of return is shown below:

The average of annual income is

= $936,000 ÷ 8 years

= $117,000

And, the average investment is

= ($1,200,000 + $100,000) ÷ 2

= $650,000

Now the average rate of return is

= $117,000 ÷ $650,000

= 18%

Answer:

c. Internal Service Fund

Explanation:

Internal Service Fund -

It refers to the sum of amount required to track the motion of any goods and services from one department to another , is referred to as internal service fund .

The amount spend on the internal service fund is used to determine the complete cost of providing the services and goods .

For example , maintenance is an example of the internal service fund .

Hence , from the given information of the question ,

The correct answer is c. Internal Service Fund .

Answer:

Tariffs and import quotas generally reduce economic welfare.

Explanation:

The vast majority of economists (over 90% according to the University of Chicago) agree that tariffs and import quotas generally reduce economic welfare. This is perhaps the normative statement in which economists agree the most.

The reason why is because tariffs and import quotas only benefit a small fraction of domestic producers, to the dismay of a larger number of consumers who end up having to pay higher prices for consumer goods.

Answer:

$ 142 375

Explanation:

Thinking process:

Let the composite rate be given by the formula:

where

A = amount after interest

= interest rate

= interest rate

t = time

n = number of times (per year)

Therefore, this gives: