Answer:

Canadian dollar - Bills are often differentiated by size for the visually impaired. Larger denominations in Australia, for instance, are both taller and wider with strong contrasting colors. Euros also follow this logic, while larger notes – like the €200 and €500 – feature tactile marks too. The U.S. and Canadian dollars are currently the only major currencies with same-size notes. The Canadian dollar, however, features tactile marks on the upper righthand corner of bills, and the notes are also different colors to aid the visually impaired. While most other countries are ahead of the U.S. in making their currencies more accessible for the visually impaired, that may soon change with a new proposed $10 bill that would be the first U.S. dollar to feature tactile markings.

Answer:

Explanation:

1. What is the partial effect of expendA on voteA?

ΔvoteAΔexpendA=β2+β4expendB→0.0382809+−6.63e−6expendB

2. Is the expected sign for b4 obvious?

Yes because the expendB alone is a negative and expendA is a positive leaving B4 to be a negative number .

Answer:

B, 195750

Explanation:

Let's first figure out the manufacturing overhead per direct labor hour

175500/13000= 13.5

So we allocate 13.5 in manufacturing overhead per direct labor hour

Let's the mulitply this by the number of actual direct labor hours

14500*13.5=195750

Answer:

The answer is Investigating Primary Sources

Explanation:

I chose this answer because According to this problem, even though it doesnt say it, the smartest way to investigate a location you want to make a business

really you would need to see the sources for it.

Mark brainlest please

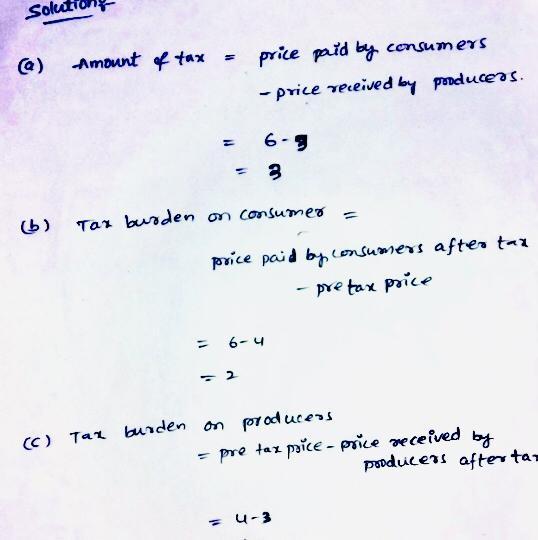

Answer:

The amount of tax will be $3

Tax Burden on consumer is $2

Tax burden on producer ( in case you want to know) will be $1

Check the image below.

Tax is equal to the difference between the price actually paid by the buyer and the price actually received by the seller. Tax= Price paid by buyer-Price received by seller Tax= $8-$5 Tax = $3 Thus the tax computed is $3 per case.