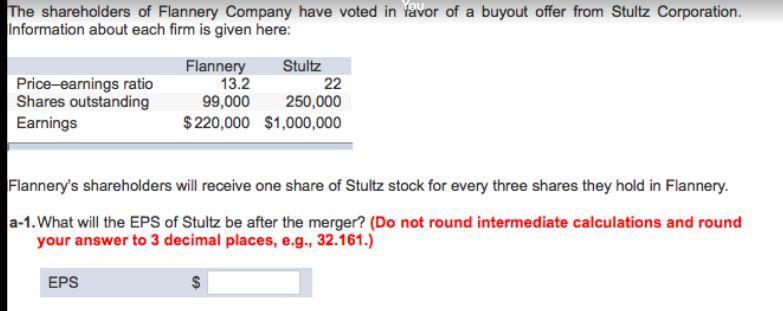

Answer:

The answer is "$4.311".

Explanation:

Calculating the EPS after the merger:

Answer:

Sequential interdependence on the line to pooled interdependence between the teams

Explanation:

Sequential interdependence occurs when a persons output is necessary for the performance of the next persons input. Perhaps the most obvious example of sequential interdependence is an assembly line.

While pooled interdependence he team accomplishes its tasks simply by bringing together everyone’s separate efforts. Like in DamierChrystern when the team work together to build the total car with the team deciding whi does what task. To be a team you need a team task — it requires that members actively work with each other to accomplish it

La cuenta de pérdidas y ganancias (P&G) es un estado financiero que resume los ingresos, los costos y los gastos incurridos durante un período específico, generalmente un trimestre o año fiscal. La cuenta de pérdidas y ganancias es sinónimo de la cuenta de resultados. Estos registros proporcionan información sobre la capacidad o incapacidad de una empresa para generar beneficios mediante el aumento de los ingresos, la reducción de los costos o ambos. Algunos se refieren al estado de ganancias y pérdidas como un estado de ganancias y pérdidas, estado de resultados, estado de operaciones, estado de resultados financieros o ingresos, estado de ganancias o estado de gastos

Answer:

Tanuja is not entitled to a QBI deduction in 2019.

Explanation:

Tanuja has QBI from her accounting firm of $540,000

W-2 wages = $156,000

Unadjusted basis of property used in the LLC = $425,000

Taxable income before the QBI deduction = $475,000

Modified taxable income = $448,000.

Her accounting firm is a "specified services" business and she and her spouse's taxable income before the QBI deduction is $475,000, which exceeds the threshold for 2019.

Answer:

Select which of the ways that entrepreneurs improve the economy is being described: As a family's basic needs are met, jobs are given to the people who help provide these needs.

new business

Explanation:

Entrepreneur improves the economy by starting a new business, they are employer of labor and improves the economy