Answer

The answer and procedures of the exercise are attached in the 2 images below.

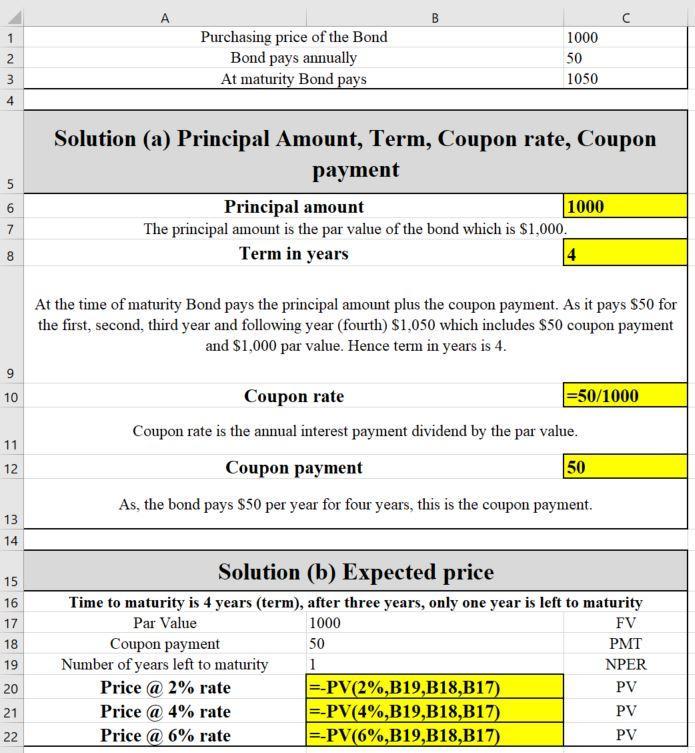

Explanation

Please consider the data provided by the exercise. If you have any question please write me back. All the exercises are solved in a 2 sheets with the formulas indications.

Answer:

Evaluate performance

Explanation:

The mbo process is a time where an employee and manager work together and sets record for a particular period of time.

This step in the mbo process is evaluation of performance. Under this step, the manager reviews the work of the employee from the question, this is what Brenda is doing with Ethan. She is evaluating his performance.

We produce this product as an example of core customer value.

The core customer value level contains the primary values, the pure blessings that every product/carrier brings to satisfy a certain want of the customer.

An organization's extra essential customers, are distinguished from the rest by way of their long-time period value to the organization.

Customer value is best defined as how a great deal a product or service is worth to a consumer. It's a measure of all of the expenses and advantages associated with a product or services. Examples consist of rate, satisfactory, and what the products or services can do for that precise person.

Learn more about the organization here: brainly.com/question/24448358

#SPJ4

Answer:

NPV = 661468 – 728000 = -66532

Explanation:

Direct Material 410

Direct Labour 100

Variable manufacturing O/H 90

Variable cost to manufacture 1 unit 600

Loss on purchase component from outside supplier

(630 – 600) * 3000 units 90000

(-) Contribution from released facility 10000

Operating Income would Decrease by 80000

Present Value of Future cash flow from Proposal X :-

PVAF for 5 years at 10% = 3.791

PVIF for 5th year at 10% = 0.621

PV of annual cash inflow (164000 * 3.791) 621724

PV of Residual value (64000 * 0.621) 39744

Present Value of Future cash flow 661468

NPV = 661468 – 728000 = -66532

Answer:

Cost of units completed = $176,528

Workings are attached:

Explanation:

Equivalent unit of production

An equivalent unit of production is an expression of the amount of work done by a manufacturer on units of output that are partially completed at the end of an accounting period. Basically the fully completed units and the partially completed units are expressed in terms of fully completed units.

Equivalent units are used in the production cost reports for the producing departments of manufacturers using a process costing system. Cost accounting textbooks are likely to present the cost calculations per equivalent unit of production under two cost flow assumptions: weighted-average and FIFO.

Conversion costs

Conversion costs is a term used in cost accounting that represents the combination of direct labor costs and manufacturing overhead costs. In other words, conversion costs are a manufacturer's product or production costs other than the cost of a product's direct materials.

Expressed another way, conversion costs are the manufacturing or production costs necessary to convert raw materials into products.

The term conversion costs often appears in the calculation of the <u>cost of an</u> <u>equivalent unit in a process costing system.</u>

For the sake of this question, we will be determining the <u>equivalent units of production:</u>

- Units completed and transferred subject to material and conversion costs

- Units in the closing inventory subject to material and conversion costs

- We will then calculate the cost per units with respect to material and conversion costs for the equivalent units.

- These cost per units will enable us to determine the cost of items completed.