Answer:

A)If interest rates decline, the prices of both bonds will increase, but the 15-year bond would have a larger percentage increase in price.

TRUE

As it has more time to maturity it will have a higher time expose to the rate therefore, will be more volatile against the rate fluctuations

Explanation:

The 10-year ond is issued at premium, above par as the coupon rate 12% is higher than market rate 10%. Each year will decrease the market value to come closer to maturity date.

The 15-year ond is issued at discount, below par as the coupon rate 8% is lower than market rate 10%. Each year will increase the market value to come closer to maturity date.

i

Explanation:

you should sell your own shirts, jackets, pants, and etc.

Answer:

The manufacturing industry helps support the global and national economies, as well as individuals and families.Manufacturing has always been on the cutting edge of technology. Relaying details about their jobs may be met with disinterest and boredom.Manufacturing affects almost everything in our lives.

The primary goal of a

firm pursuing a blue ocean strategy should be to OFFER A DIFFERENTIATED SERVICE

OR PRODUCT AT A LOW COST.<span>

<span>Blue ocean strategy is a marketing strategy which submits

that leading companies can succeed not by engaging in competition with other

companies but by systematically creating uncontested market space which are

ripe for growth. The strategy employs simultaneous pursuit of high product

differentiation and low cost, which makes competition irrelevant</span></span>

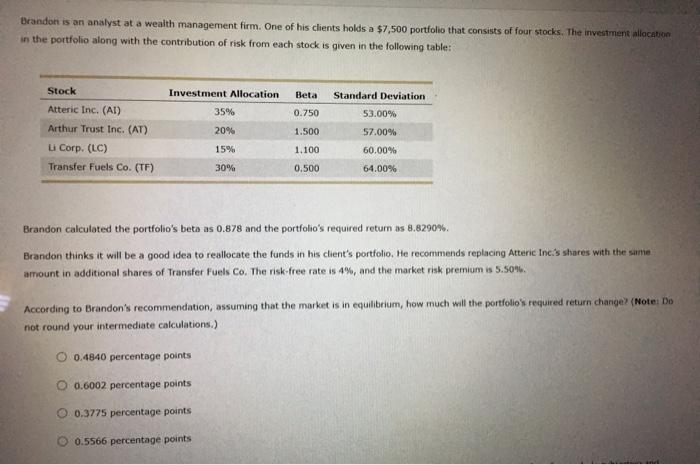

Answer:

a. 0.4840 percentage points

b. Project is overvalued

c. Required return from the portfolio would increase.

Explanation:

Note: The full question is attached as picture

New Allocation on Transfer Fuels corporation = 30%+35%

New Allocation on Transfer Fuels corporation = 65%

Beta after the new allocation = (20%*1.50) + (15%*1.10) + (65%*0.5)

Beta after the new allocation = 0.3 + 0.165 + 0.325

Beta after the new allocation = 0.79

New Required rate = Risk free rate + Beta* Market risk premium

New Required rate = 4%+ 0.79*5.5%

New Required rate = 4% + 4.345%

New Required rate = 8.345%

Hence, the change in required rate = 8.829% - 8.345% = 0.4840%

. In this case, the project is overvalued if Brandon expects 6.85%

. If Higher beta is chosen the portfolio risk would increase and required return from the portfolio would increase.