Answer and Explanation:

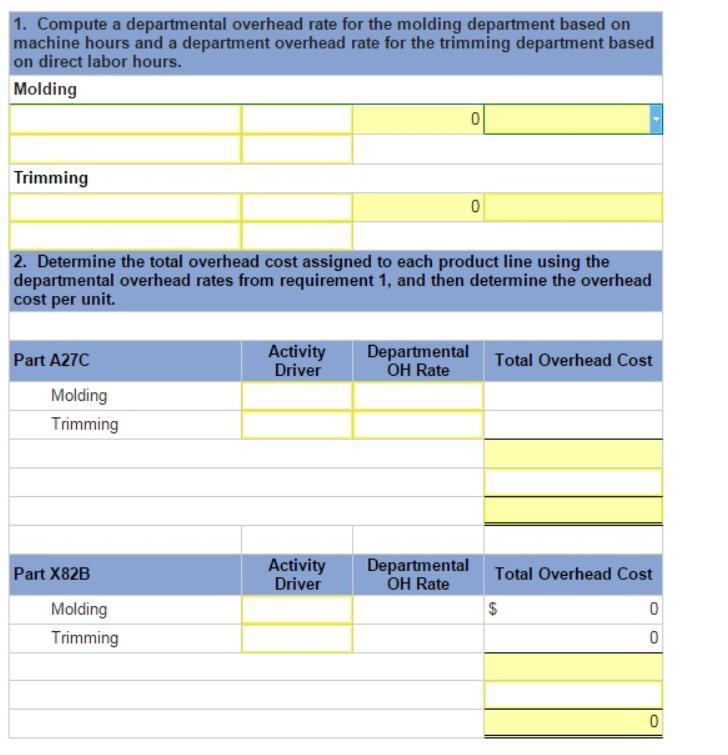

1. The computation of the departmental overhead rate for the molding department based on machine hours and for trimming department based on direct labor hours are shown below:

For molding department

= Overhead cost ÷ machine hours

= $730,000 ÷ 30,500 machine hours

= $23.93 per machine hour

For trimming department

= Overhead cost ÷ direct labor hours

= $590,000 ÷ 48,000 direct labor hours

= $12.29 per machine hour

2. Now the total overhead cost for Part A27C and Part X82B and its overhead cost per unit are as follows

Part A27C Activity Departmental For Total Overhead

Driver OH Rate each Cost

Molding Machine

Hours $23.93 Machine $122,065.57

Hour (5,100 MH × 23.93

)

Trimming Direct

Labor Hours $12.29 Direct $8,604.17

Labor Hour (700 DLH × 12.29

)

Total Overheads $130,669.74 ÷ 9,800 units

Overhead per unit $13.33

Part X82B Activity Departmental For Total Overhead

Driver OH Rate each Cost

Molding Machine

Hours $23.93 Machine $24,413.11

Hour (1,020 MH × 23.93

)

Trimming Direct

Labor Hours $12.29 Direct $43,020.83

Labor Hour (3,500 DLH × 12.29)

Total Overhead $674,33.95 ÷ 54,500 units

Overhead per unit $1.24