Answer:

It can help you to understand ideal customers and the target audiences

Explanation:

Market segmentation is important due to the following reasons:

1. It can help you to understand ideal customers and the target audiences

2. Market segmentation helps to provide content to the target people in the proper way.

3. Market segmentation allows companies to understand customer's needs, wants, preferences and behaviors.

Market Research

Explanation:

In a global business, <u>The firm often goes into uncharted territories for themselves and takes heavy risks in places unknown to them.</u> In such a situation market research done right is the best thing a firm can hope for apart from all other things.

A market not suitable for their products will simply not be beneficial no matter how everything else works out.

For example,<u> McDonald's setting up operations in India made its menu suit the Indian taste pallet and was able to carve out a market share</u> while other food chains were not as quick to do it.

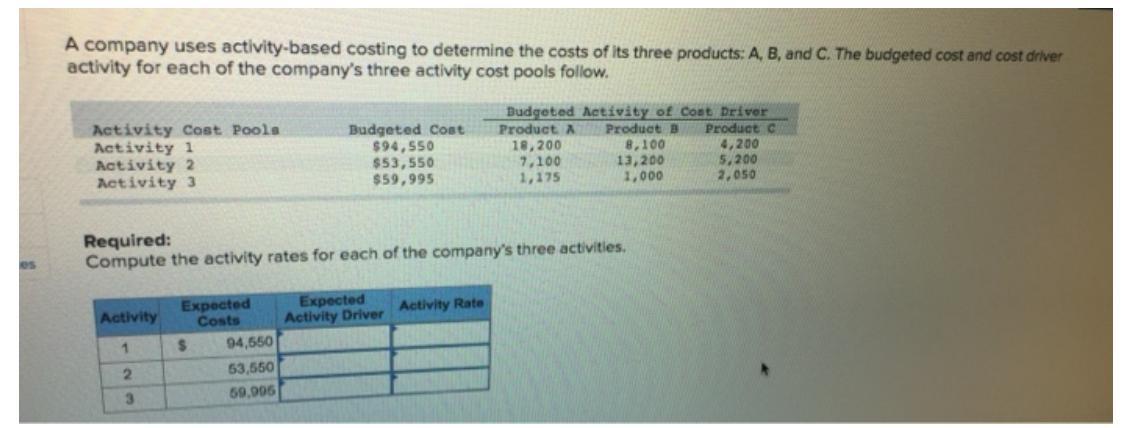

Answer:

$3.10 ; $2.10 and $14.20

Explanation:

The computation of the activity rates is shown below:

For Activity 1

= Budgeted cost ÷ Total budgeted activity of cost driver

= $94,550 ÷ (18,200 + 8,100 + 4,200)

= $94,550 ÷ 30,500

= $3.10

For Activity 2

= Budgeted cost ÷ Total budgeted activity of cost driver

= $53,550 ÷ (7,100 + 13,200 + 5,200)

= $53,550 ÷ 25,500

= $2.10

For Activity 3

= Budgeted cost ÷ Total budgeted activity of cost driver

= $59,995 ÷ (1,175 + 1,000 + 2,050)

= $59,995 ÷ 4,225

= $14.20

Answer:

Explanation:

Current price = Annual coupon*Present value of annuity factor(7.2%,12)+$1000*Present value of discounting factor(7.2%,12)

1142.60=Annual coupon*7.85871162+$1000*0.434172763

1142.60=Annual coupon*7.85871162+434.172763

Annual coupon=(1142.60-434.172763)/7.85871162

Annual coupon = $90.14

Coupon rate=Annual coupon/Face value

=$90.14/$1000

=9.01%

Answer:

Formal selection principle..

Explanation:

- Max Weber gave 5 principles of the bureaucratic structure as the division of labor, hierarchy of authority, and the framework of rules, impersonality a formal selection.

- As kate is in middle management of a large organization she at the center of the hierarchy of the organization and believes that the subordinates can help in the decision making the process. This will lead to the creation of innovative ideas, reducing wastages of resources and time.