Market Equilibrium is when the supply and demand curves intersect, the market is in equilibrium. This is where the quantity demanded and quantity supplied are equal. The corresponding price is the equilibrium price or market clearing price, the quantity is the equilibrium quantity.

Answer:less than 5% or equal to 5%

Explanation:

Due to it's high credit rating the populace will have confidence in him and it will not need to increase it's rate to attract investors.

This is similar to a government issuing treasury bill which rate of return will be less than the banks or other similar institution

Answer:

Accounts Payable 15,000

Prepaid Rent 39,000

Explanation:

<u><em>Assets:</em></u>

Cash 25,000

Supplies 10,000

Prepaid Rent X?

Equipment 90,000

Land 150,000

Total Assets = 290,000

We subtract from the total assets the know values to get the unknow which is, prepaid rent:

290,000 - 150,000 - 90,000 - 10,000 - 25,000 = 15,000 prepaid rent

Then laiblities + equity = total assets

so we use the same idea;

Liabilities

Accounts Payable X?

Salaries Payable 12,000

Notes Payable 99,000

Total liabilities Y?

Equity

Common Stock 40,000

Retained Earnings 100,000

Total equity 140,000

Total Liab + SE 290,000

290,000 - 140,000 = total liab = 150,0000

then AP

150,000 - 99000, - 12,000 = 39,000

Answer:

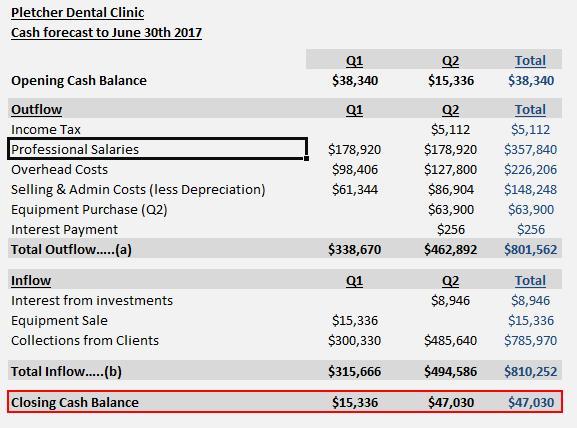

The closing cash balance in this question is $47,030. Which is over the minimum cash requirement the business hopes to have.

Explanation:

In preparing a cash budget, focus should be given to both real cash creating revenues/ income and cash creating expenses or acquisitions.

If there is no cash implication in the specified transaction it should be ignored. For example depreciation, or a transaction for which payment or receipt of cash occurs outside the budget period.

The closing cash balance in this question is $47,030. Which is over the minimum cash requirement the business hopes to have.

The breakdown of the budget is detailed in the attached file.

Answer:

2- A. Establish ground rules

3- D. Top management’s requirements.

Explanation:

2- An effective team is a well-integrated team, where the flow of information occurs effectively and where each member feels equally respected and an important part of the team, being able to contribute with ideas and feedback.

Therefore, for there to be cohesion and improvement of the team's performance, it is necessary to establish basic rules, to guide the behavior and actions of members and for there to be equality among all, in order to avoid conflicts and organize work.

3- to guide the process of the performance improvement team, the most important alternative is the requirements of senior management.

It is the managers who will coordinate, monitor and guide the action plans and develop the fundamental requirements for the execution of the business actions that will lead to the fulfillment of the objectives and goals.