Answer:

Current or potential creditors — like credit card issuers, auto lenders and mortgage lenders — can pull your credit score and report to determine creditworthiness as well. Credit history is a major factor in determining (a) whether to give you a loan or credit card, and (b) the terms of that loan or credit card.

Explanation:

Simplify this it may help.

Answer:

x1 + x2 + x3 + x4 + x5 + x6 + x7

Explanation:

Formulating the problem as an LP

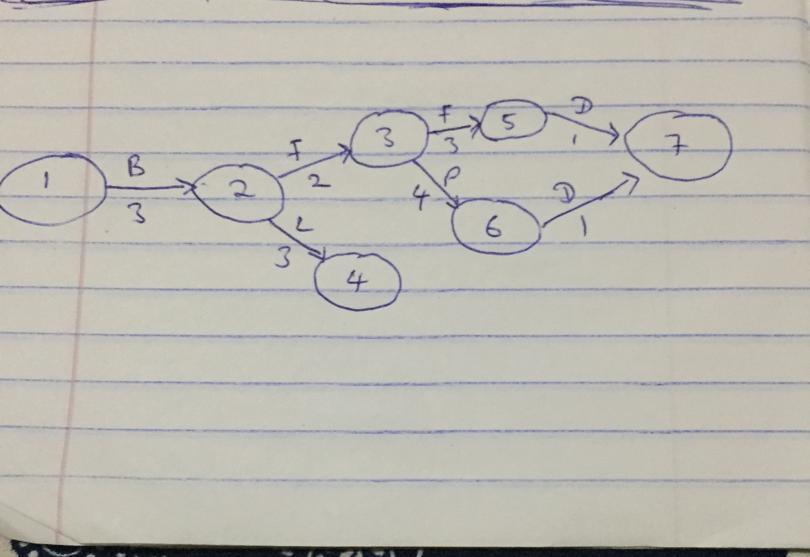

Attached below is an AOA diagram and the completion time of each task is indicated in the diagram, The diagram was based on the conditions given for the completion of each task accordingly.

To complete the project as early as possible we will have assume

x1, x2, x3, x4, x5, x6, and x7 to be the times taken to complete each node

hence the earliest time taken to complete the project

= x1 + x2 + x3 + x4 + x5 + x6 + x7

when : x2 - x1 ≥ 3

x3 - x2 ≥ 2

x4 - x2 ≥ 2

x5 - x3 ≥ 3

x6 - x3 ≥ 3

x7 - x5 ≥ 1

x7 - x6 ≥ 1

also : x1, ............ , x7 ≥ 0

Answer:

The appropriate solution is:

(a) 2828 cases each time

(b) $4005656.85

(c) $3609800

Explanation:

The given values are:

Annual demand,

D = 200,000 cases

Per case cost,

C = $20

Carrying host,

H =

= $

Ordering cost,

S = $40

(a)

The economic order quantity will be:

⇒

On substituting the values, we get

![=\sqrt{[\frac{(2\times 200000\times 40)}{2} ]}](https://tex.z-dn.net/?f=%3D%5Csqrt%7B%5B%5Cfrac%7B%282%5Ctimes%20200000%5Ctimes%2040%29%7D%7B2%7D%20%5D%7D)

(b)

According to the question,

The annual ordering cost will be:

=

=

=  ($)

($)

The annual carrying cost will be:

=

=

=  ($)

($)

The annual purchase cost will be:

=

=

=  ($)

($)

Now,

The total inventory cost will be:

=

=  ($)

($)

(c)

According to the question,

Order quantity,

Q = 10000 cases

Per case cost,

C = $18

Carrying cost,

H =

=

The annual ordering cost will be:

=

=

=  ($)

($)

The annual carrying cost will be:

=

=

=  ($)

($)

The annual purchase cost will be:

=

=

=

Now,

The total cost of inventory will be:

=

=  ($)

($)

Answer:

$800

Explanation:

Fred and Lucy's itemized medical expenses are:

doctor and dentist bills + hospital expenses $9,200

<u>minus reimbursements ($4,400) </u>

unreimbursed expenses $4,800

Health insurance premiums $5,000

<u>Prescribed medicines and drugs $3,000 </u>

Total medical expenses $12,800

<u>minus 10% of AGI = 10% x $120,000 ($12,000) </u>

Deductible medical expenses $800

Contribution to qualified Health Savings Accounts are deducted directly from the AGI, and should not be included as medical expenses.

Answer:

State orientation

Explanation:

The state orientation is the term which is defined as the inability of the person to regulate the behavior, emotions and thoughts. In short, it means that the individuals or the person unable to modify their state of mind, their uncertainty, dejection, anxiety and confusion.

Under this scenario, Jean who whenever accompany their friends on shopping, she could not able to resist herself from buying the products on sales and spend a lot more than budget, so, it could be concluded that she is state orientated.