Answer:

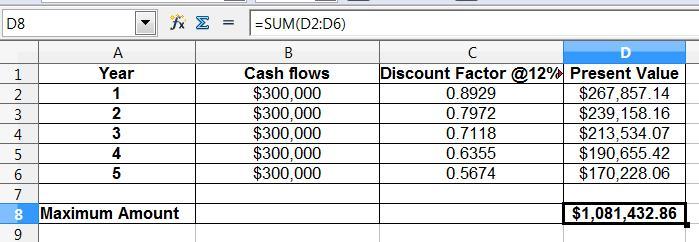

Hence, the the maximum amount the company could invest in the project is $1081432.86 and yes, the project should be accepted as the value is greater than initial investment.

Therefore, the correct option is b. $1,081,434

Explanation:

Here, maximum amount means the sum of present value of all cash inflows

So,

Present value = all Year cash inflows × Discounted factor of each year

where,

Year 1, year 2, year 3, year 4, and year 5 have same cash flows i.e. $300,000

But the discounted factor is different in each year

The calculation of discounted factor = 1 ÷ (1+0.12) ^ 1

where,

0.12 = rate

^1 = for year 1, ^2 = for year 2 and so on.

The discounted rate for year 1, , year 2, year 3, year 4, and year 5 is 0.8929

, 0.7972

, 0.7118

, 0.6355

, 0.5674 respectively.

Now, multiply the cash flow amount with discounted rate for each year to get presented value of all years.

Year 1 = $300,000 × 0.8929 = $267,857.14

Year 2 = $300,000 × 0.7972 = $239,158.16

Year 3 = $300,000 × 0.7118 = $213,534.07

Year 4 = $300,000 × 0.6355 = $190,655.42

Year 5 = $300,000 × 0.5674 = $170,228.06

Then, sum all the presented values of all year to get maximum amount

= $267,857.14 + $239,158.16 + $213,534.07 + $190,655.42 + $170,228.06

= $1,081,432.86

So, we attached the sheet for better understanding.

Hence, the the maximum amount the company could invest in the project is $1081432.86 and yes, the project should be accepted as the value is greater than initial investment.

Therefore, the correct option is b. $1,081,434