Answer:

a. $16.

Explanation:

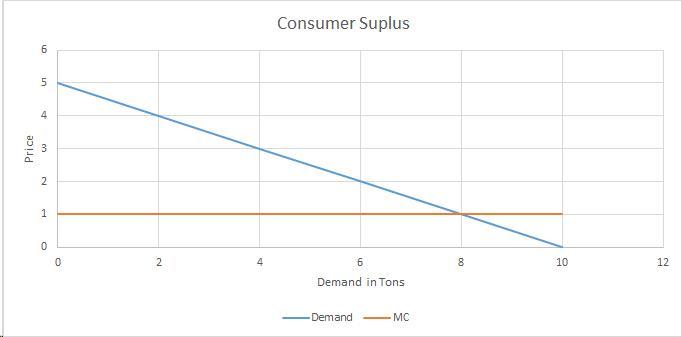

the firm offer a price where marginal revenue = marginal cost

We have to solve at which quantity the price is $1.

There, the marginal revenue would match the marginal cost.

1 = 5 - 0.5q

q= (5 -1) /0.5 = 4/0.5 = 8

Now, we solve or the price at which quantity is zero:

p = 5 - 0.5(q) = 5 - 0 = 5

With that we can now solve for the consumer good as the area of the triangle above the marginal cost and below the demand function

(see attached graph)

8 x (5-1) / 2 = 16

Answer:

The after-tax MARR is 13.26%

Explanation:

After - tax MARR = Before tax MARR*(1 - tax rate)

= 17%*(1 - 22%)

= 13.26%

Therefore, The after-tax MARR is 13.26%

Answer:

Option A. Variable costs of $56,700 and $43,900 of fixed costs

Explanation:

Given:

Jase Manufacturing Co.'s static budget at 7,800 units of production includes;

Direct labor = $39,000

Electric power = $3,120

Total fixed costs= $43,900

Variable costs = [$(39,000 + 3,120) ÷ 7800] × 10,500= $56,700

Fixed costs = $43,900

Answer:

the extent to which consumers are familiar with the distinctive qualities or image of a particular brand of goods or services.

Explanation:

google