Answer:

To cover budget imbalances, governments borrow money

Explanation:

A government's national debt grows every time it borrows money.

The answer is B a hospital

This first-mover advantage occurs when a company can significantly increase its market share by being first with a new competitive advantage.

<h3>What are the important competitive advantage?</h3>

Competitive advantage will give a market an edge over another market.

This is because market are mostly competitive in nature and when an individual is performing better in terms of profit and reduced expenses then the Market is at advantage.

Therefore, this first-mover advantage occurs when a company can significantly increase its market share by being first with a new competitive advantage.

This first-mover advantage occurs when a company can significantly increase its market share by being first with a new competitive advantage.

Learn more on competitive advantage below

brainly.com/question/14486110

#SPJ1

Try using this website:

https://smallbusiness.chron.com/10-important-business-objectives-23686.html

Answer

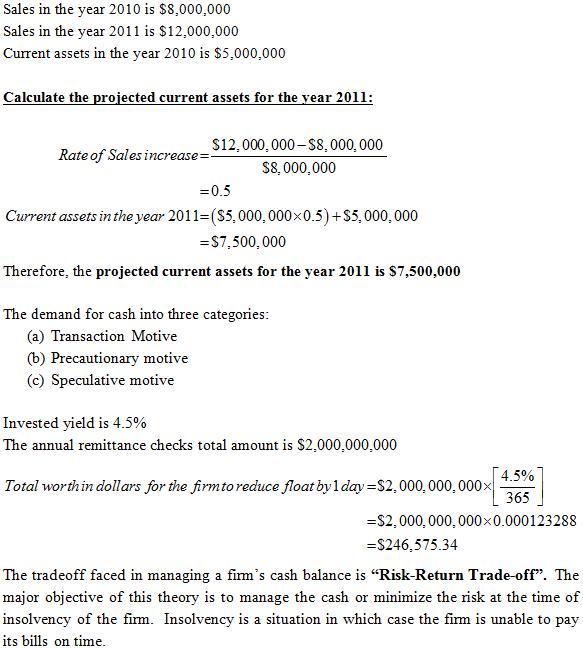

The answer and procedures of the exercise are attached in the following archives.

Step-by-step explanation:

You will find the procedures, formulas or necessary explanations in the archive attached below. If you have any question ask and I will aclare your doubts kindly.