Answer:

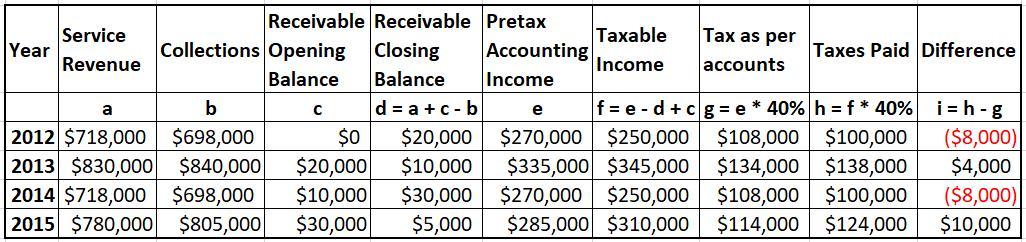

Please see the attached Snapshot for a schedule showing service revenue receivable and below are the journal entries for the year 2013, 2014 and 2015 on Income Taxes.

Explanation:

1. 2013 Journal Entry

Alsup Consulting

Dated: December 31, 2013

Debit: Tax Expense $134,000

Debit: Deferred Tax Liability $4,000

Credit: Income Tax Payable $138,000

<em>To record Income Tax Payable.</em>

2. 2014 Journal Entry

Alsup Consulting

Dated: December 31, 2014

Debit: Tax Expense $108,000

Credit: Income Tax Payable $100,000

Credit: Deferred Tax Liability $8,000

<em>To record Income Tax Payable.</em>

3. 2015 Journal Entry

Alsup Consulting

Dated: December 31, 2015

Debit: Tax Expense $114,000

Debit: Deferred Tax Liability $10,000

Credit: Income Tax Payable $124,000

<em>To record Income Tax Payable.</em>