Answer:

b. 10.426%

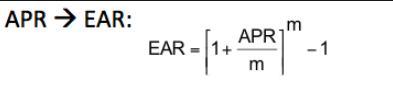

Explanation:

Using the attached formula, convert the nominal rate to effective annual rate

<em>m</em> in the formula is the number of compounding periods per year; 12/2 = 6 in this case.

APR is the nominal rate which is 10%.

Next, plug in the numbers to the formula as shown below;

EAR = ![[1+\frac{0.10}{6}]^{6} -1](https://tex.z-dn.net/?f=%5B1%2B%5Cfrac%7B0.10%7D%7B6%7D%5D%5E%7B6%7D%20-1)

EAR = 1.10426-1

EAR = 0.10426 or 10.426% as a percentage

Hence choice B is correct.

<span>This is an example of industry competition. Industry competition is a rivalry between companies in the same market who offer similar products or services. These industries compete for potential customer's money and use a variety of means to make sure they are the one a consumer chooses to do business with. They can use advertising to try and attract consumers or offer lower prices, but the most important thing is to provide a good product or service.</span>

No the electronic devices where made to text and easier to text