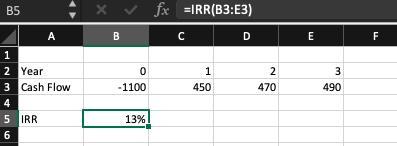

Answer:

13%

Explanation:

To solve for the IRR we first need the formula

where NPV is the net present value,  is the cash flow in period t, and r is the IRR (internal rate of return)

is the cash flow in period t, and r is the IRR (internal rate of return)

Solving this polynomial can be quite cumbersome. Thankfully excel has a built in function that we can take advantage of call IRR

As shown in the screen shot we write the cash flow, with the first one with the negative sign. Then we call the IRR function selecting the cells with our Cash Flow values and excel will return the IRR. In this case is 13%

Answer:Technological advancements.

Explanation: Technological advancement is the overall improvement in the Manufacturing, Organisation, coordinating and use of technology in order to meet the growing needs of Man. Technological advancements can be in different fields such Medical,trade/commerce, Manufacturing etc.

THE ABILITY OF THE GERMAN BREWERY BEING ABLE TO ORDER STATIONERIES FROM ENGLAND USING AN ONLINE FORM IS AN EXAMPLE OF TECHNOLOGICAL ADVANCEMENT.

Answer:

B. Coordinates production and sales efforts.

C. Takes into account current inventory, confirmed orders, and scheduled production.

Explanation:

Available to promise is a feature in businesses where the person in charge links up the available goods to the customer's demands. It is a coordination of production and sales.

The personnel representing the business checks the current level of production and tries to see if the current level of production or even the scheduled production can meet up with customer's demands. Some computer software are used to perform this operation in real-time.

And she was able to do just that because she is rich, right?

Answer:

True

Explanation:

unstructured organizational can as well be regarded as "decentralized organization" it can can simply explained as one with little bureaucratic or hierarchical structure. In an unstructured organizational decision, the decision maker needs to make provision for insight and evaluation for the problem definition, because in this unstructured organizational decision every decision is crucial and there is no or little procedures to follow in making these decisions. It should be noted that in unstructured organizational decisions, few or no procedures to follow for a given situation can be specified in advance.