So this question is too complicated for a forum like this to answer all parts.

I can help with a few of the first ones.

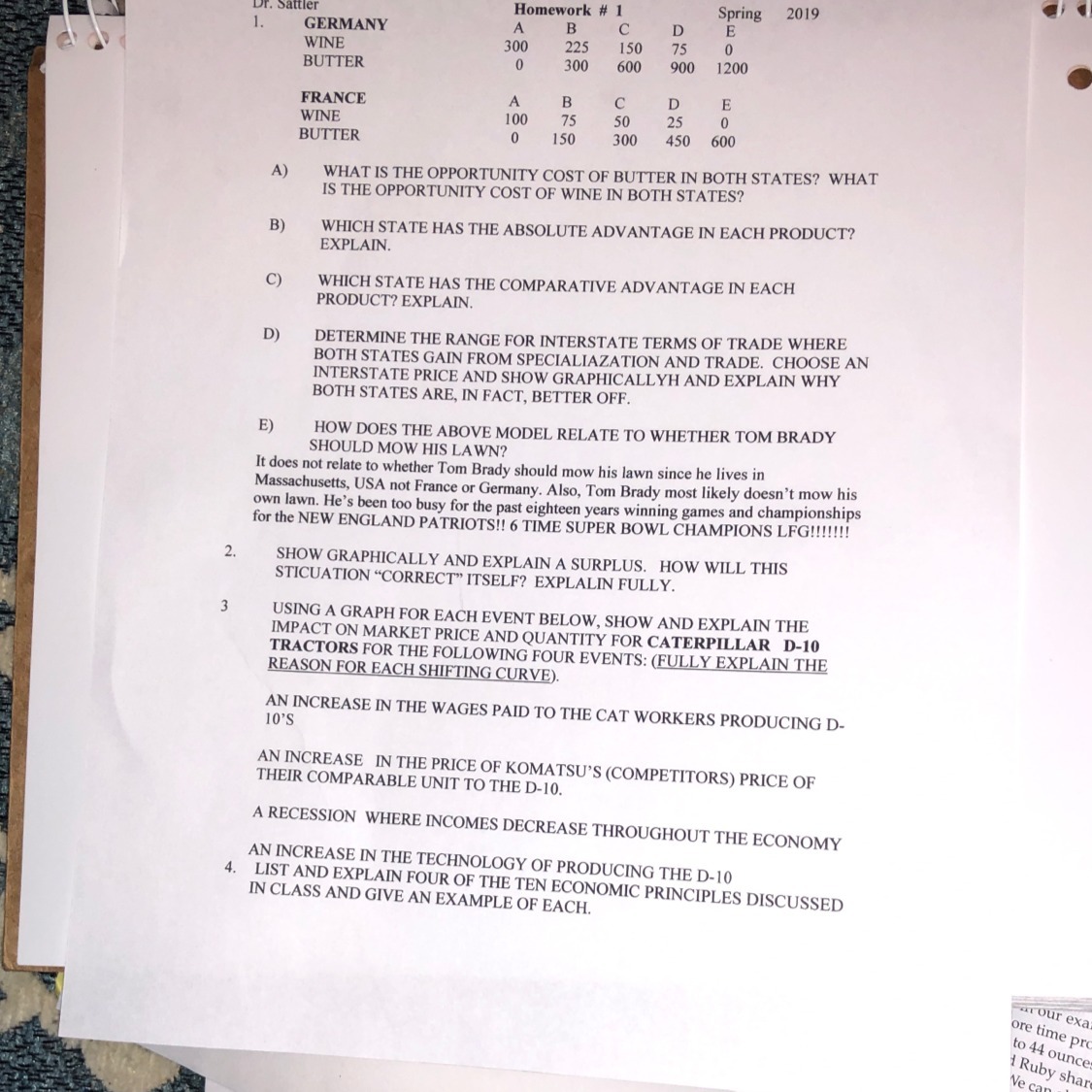

A. To figure opportunity costs, you find the ratio between producing all wine versus producing all butter.

In this case Germany: if Germany only produces wine they make 300 units. If they only make butter they make 1200 units. So the opportunity costs would be 1200/300 or 4. For every one unit of wine, you give up 4 units of butter.

B. Absolute advantage is the country the can produce the most units overall.

C. Comparative advantage is the country that has the capability of producing the most of one specific product. I.E. who can produce the most butter or wine.

D. I cannot draw that here.

E. I would rethink the answer on your sheet. Think about the above example of opportunity cost. Is it worth Tom Brady giving up time thinking about football to mow his lawn? How much opportunity cost would be there?