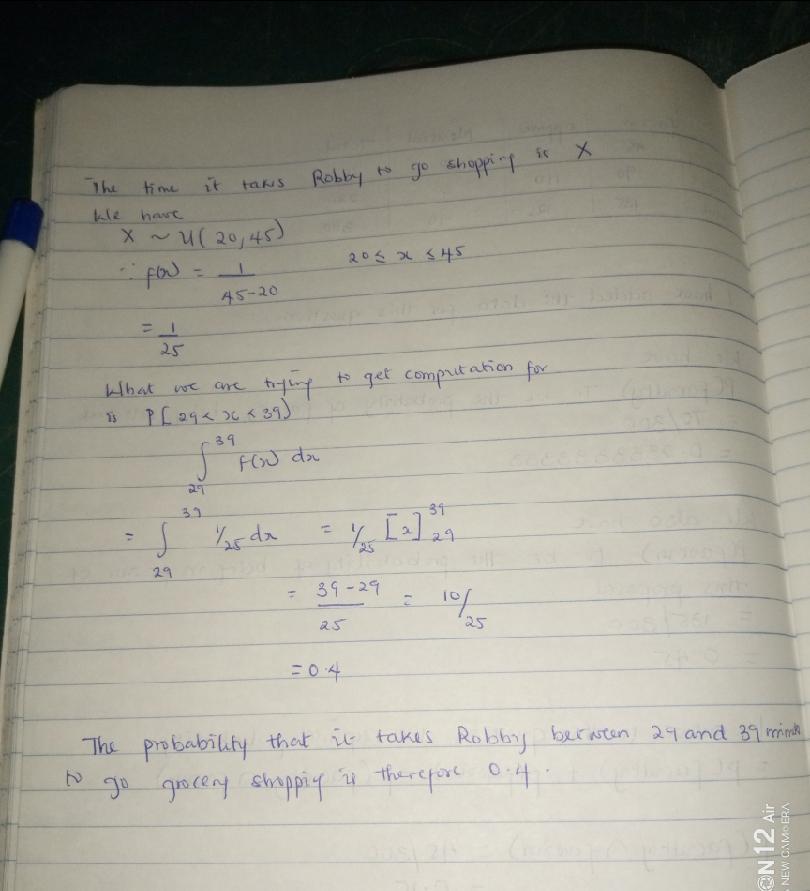

Answer:

0.4

Explanation:

This problem has been solved using the method of integration.

We are required to solve for the probability that it takes Robby between 29 and 39 minutes to go grocery shopping

= X~U(20,45)

= 1/45-20

= 1/25

Then we get computation for p[29<x<39]

When we take the integrals with x = 1/25

We get

Probability that it takes Robby between 29 and 39 minutes to go shopping to be 0.4

Answer:

9.37

Explanation:

The computation of LCL for a control chart is shown below:-

Sample Obs 1 Obs 2 Obs 3 Obs 4 Mean observation Range

1 10 12 12 14 12 4

2 12 11 13 16 13 5

3 11 13 14 14 13 3

4 11 10 7 8 9 4

5 13 12 14 13 13 2

For computing the mean observation and range we will use the below formulas

Mean observation = ( Obs 1 + Obs 2 + Obs 3 + Obs 4) ÷ 4

Range = Highest value - Lowest value

= ( 12 + 13 + 13 + 9 + 13 ) ÷ 5

= ( 12 + 13 + 13 + 9 + 13 ) ÷ 5

= 12

= ( 4 + 5 + 3 + 4 + 2 ) ÷ 5

= ( 4 + 5 + 3 + 4 + 2 ) ÷ 5

= 3.6

Since we found the value of A2 with the help of constants table for control charts for a 4 subgroup size.

A2 = 0.729

12 - 0.729 × 3.6

= 9.37

Answer:

d. It is best measured using the statistic variance inflation factor (VIF).

Explanation:

Multicollinearity is an important issue in multiple regression model, having many independent/ explanatory variables. Multicollinearity is the situation in which two or more independent variables are highly correlated. It is problematic because it increases the standard error of independent variable coefficient & undermines its statistical significance

Variance Inflation Factor [VIF] is a check & corrective measure of multicollinearity.

- VIF as a multicollinearity check : It quantifies the correlation between one explanatory variable with other explanatory variables.VIF = 1 implies there is no multicollinearity (correlation between independent variables); VIF upto 5 implies there is moderate multicollinearity (correlation between independent variables). VIF > 5 implies high multicollinearity (correlation between independent variables)

- VIF as a multicollinearity correction : Calculating

= σ^2 /

= σ^2 / ![[TSS j (1 - R^2j)]](https://tex.z-dn.net/?f=%5BTSS%20j%20%281%20-%20R%5E2j%29%5D) ; where TSS = total sum of square of variable j , σ^2 = j variance, R^2 j = R^2 from regressing all other independent variable on variable j

; where TSS = total sum of square of variable j , σ^2 = j variance, R^2 j = R^2 from regressing all other independent variable on variable j

Answer:

option 14.92%

Explanation:

Data provided in the question;

Expected annual dividend to be paid = $0.65

Expected growth rate = 9.50%

Walter’s stock currently trades = $12.00 per share

Now,

Expected rate of return =  + Growth rate

+ Growth rate

or

Expected rate of return =  + 9.50%

+ 9.50%

or

Expected rate of return = ( 0.054167 × 100% ) + 9.50%

or

Expected rate of return = 5.4167% + 9.50%

or

Expected rate of return = 14.9167 ≈ 14.92%

Hence, the correct answer is option 14.92%