Answer: Adverse Selection.

Explanation:

The above situation described Adverse Selection because Adverse Selection refers to a situation where there is information asymmetry between buyers and sellers of a good or service. This means that a party involved has more information about the transaction than the other and this can lead to the person who has more information engaging in a transaction that is sure to benefit them at the expense of the person they are transacting with. A serious example is one of life insurance. Perhaps if a person knows that they will be dying soon but it won't show up on all medical scans and tests, they will get the life insurance and claim on it when they die. They had more information than the seller.

In the above scenario, Tim can make all the assumptions he wants to make but the fact is he simply will.not know what defects the television has because he is not the seller.

It is applaudible that he is approaching with caution though. He at least has a higher chance of success.

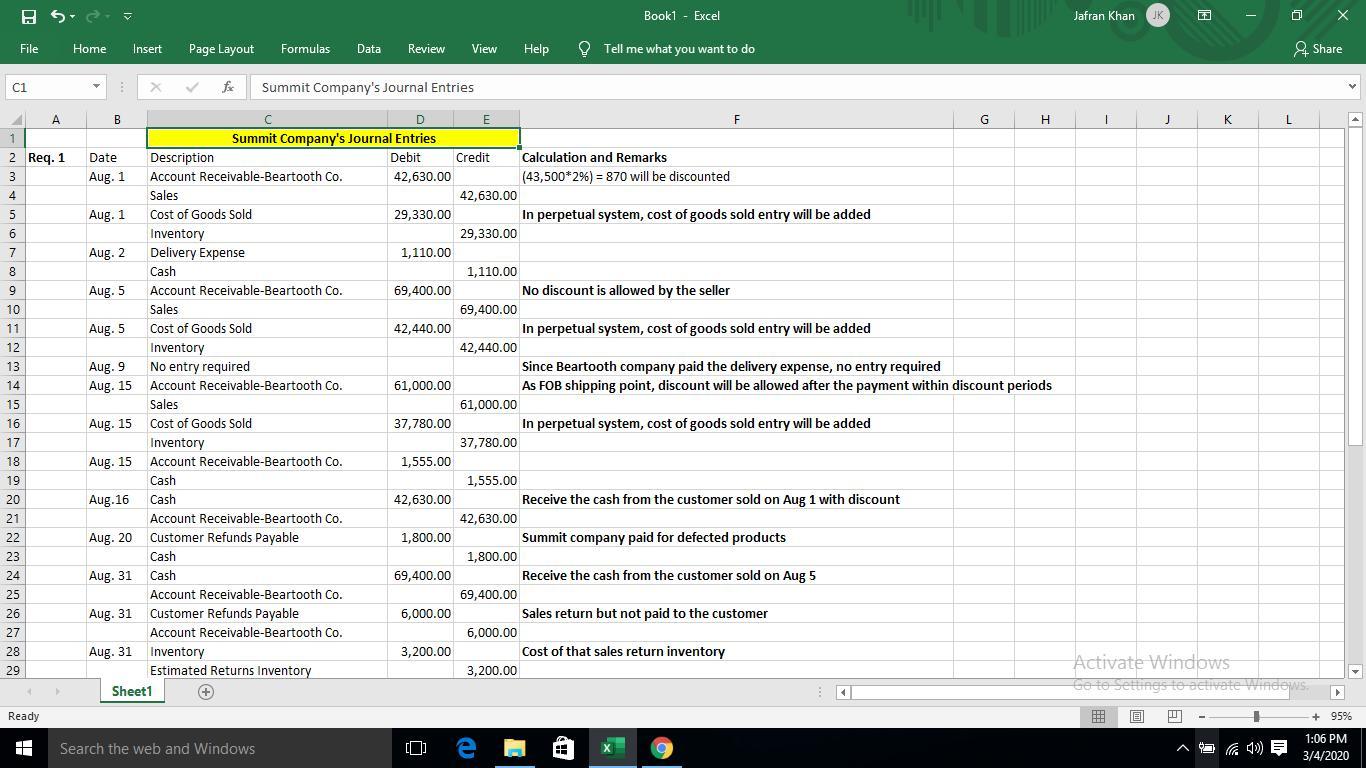

Answer:

See explanation section

Explanation:

See the following images to get the appropriate answer.

Answer:D. Increasing the allowance for sales returns by an amount that is less than the actual returns recognized for the period may indicate either the company is attempting to increase profit for the period or its estimates that less of its products will be returned in the future.

Explanation:Sale returns is a term used in Financial accounting to mean the adjustments made to the sales due to the actual return of a mechandise by a customer who has made purchase of that mechandise previously.

SALES RETURNS ARE USUALLY RECORDED IN THE "SALES RETURN AND ALLOWANCE" RECORDED IN THE INCOME STATEMENT AS A DEDUCTION.

For a successful sales return to be achieved,it must be accompanied with actual product or mechandise return and refund.

Answer:

Interest rates would rise.

Explanation:

There would be a decrease in the amount of loanable funds borrowed.

if the government were to increase the tax on interest income, a reduction in the amount of funds borrowed would happen because the cost of borrowing would then become higher and people would have to pay more than they would have paid for every amount borrowed

Answer:

true

Explanation:

Gross domestic product is the sum of all final goods and services produced in an economy within a given period which is usually a year.

GDP can be calculated using the expenditure approach.

GDP = Consumption spending + Investment + Government Spending + Net Export

GDP of the US for the 3rd quarter of 2019 was $5,385,635 million

I hope my answer helps you