Answer:

Elastic which is more than 1.

Explanation:

Price elasticity of demand is the responsive relationship of quantity demanded when compared to price. It measures how much change there would be in demand if Price were to change.

The raise in prices yielded a fall in revenue because the demand for tickets was elastic. (More than 1)

An elastic demand means that a small change in price will cause a more than proportionate change in qty demanded and hence with an increase in price, far less people purchased the ticket.

An inelastic demand however would have caused less people to give up tickets and raised overall revenues.

Hope that helps.

Answer:

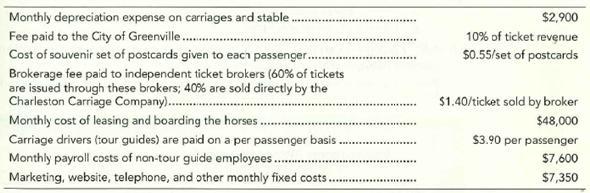

1) Colt Carriage Company

Income Statement

For the month ended April 202x

Revenues:

- Adults passengers $186,300

- Children $81,000

- Total revenues $267,300

Variable costs:

- City fees $26,730

- Souvenirs $7,425

- Brokerage fees $11,340

- Carriage drivers $52,650

- Total variable costs <u>$98,145</u>

Contribution margin $169,155

Period costs:

- Depreciation $2,900

- Horse leases $48,000

- Marketing expenses $7,350

- Payroll expenses $7,600

- Total period costs <u>$65,850</u>

Operating profit $103,305

2) If the total amount of passengers increase by 10%, then all variable costs will increase by 10% except brokerage fees which would increase only by 6%. Revenues should also increase by 10%. Period costs should not change.

Contribution margin should increase by 10.29% and operating profit would increase by 16.81%.

Explanation:

since the information is not complete, I looked it up:

Revenues

13,500 passengers:

8,100 x $23 = $186,300

5,400 x $15 = $81,000

total $267,300

variable costs:

fees paid to the city 10% of total revenue

souvenirs $0.55 per passenger

brokerage fees 60% of total tickets x $1.40

carriage drivers $3.90 per passenger

fixed costs:

depreciation $2,900

horse leases $48,000

marketing expenses $7,350

payroll expenses $7,600

Answer:

a.

Explanation:

Operating Activities records the cash transactions involved in the operations of the business are recorded under ‘operating activities’ in the cash flow statement.

Examples: Revenue earned, expenses incurred etc.

There are two methods to prepare the cash flow statement. The only difference between both the methods is the way of presenting cash flow from operating activities.

The two methods of presenting cash flow statement are:

- Direct method: Operating activities section under direct method reports the amount of cash received and paid by the company during the period.

- Indirect method: Operating activities section under indirect method reports the net income and later adjusts the transactions to convert it to cash basis of accounting.

Depreciation expense is a non-cash operating expense. Thus, it is added back to the net income to derive net cash inflow from operating activities section of the cash flow statement.

Answer: True

Explanation: The retained earnings are recorded after closing the accounts of the income statement, the surplus called profit or the missing called loss is transferred to equity through the non-distributed profit item.

This undistributed profit account also closes during the accounting period, to clarify how much was generated in a period, they are not like the balance sheet accounts that are cumulative.

Answer:

The labor efficiency variance for this last pay period was $1,200 Favorable.

Explanation:

In order to calculate Dreary's labor efficiency variance for this last pay period, we have to calculate first the standard hours allowed for actual work using the following formula:

Standard hours

allowed for actual work= (

<u>Total number of applications

)</u> × number of

Standard number of applications hours worked

= <u>(2.500 applications)</u>× 8 hours

10 applications

=2,000 hours

After having calculated the Standard hours allowed for actual work, we can calculate the labor efficiency variance using the following formula:

labor efficiency variance= (Actual hours worked-Standard hours allowed for actual work)× standard rate

= (1,920-2,000)×$15

=-$1,200

The Labor efficiency variance is $1,200 Favorable.

<u></u>