<h2>Evaluating one's contribution gets employee thinking about their performance.</h2>

Explanation:

Self-appraisal is one of the best method to assess themselves of what kind of contribution that he has made to the company to grow.

He can also look back about the opportunities that the company has given to him to perform.

This actually,

- speaks for results

- gets the chance to do peer review

- an exercise to grow in terms of career

- list out the achievements of self

- contribution done by the self

So the chosen statement supports Dylan's idea.

Answer:

$3,173.63

Explanation:

For computing the price of the bond we need to apply the present value i.e to be shown in the attachment

Given that,

Future value = $3,000

Rate of interest = 4.8% ÷ 2 = 2.4%

NPER = 25 years × 2 = 50 years

PMT = $3,000 × 5.2% ÷ 2 = $78

The formula is shown below:

= -PV(Rate;NPER;PMT;FV;type)

So, after applying the above formula, the price of the bond is $3,713.63

Answer:

$3.28 per ton

Explanation:

Total value = Land + Estimated restoration costs

= $7,440,000 + 1,440,000

= $8,880,000

Value for depletion = Total value - Salvage value

= $8,880,000 - $940,000

= $7,940,000

Per ton Depletion:

= Value for depletion ÷ Recoverable reserves

= $7,940,000 ÷ 2,420,000 tons

= $3.28 per ton

Answer:

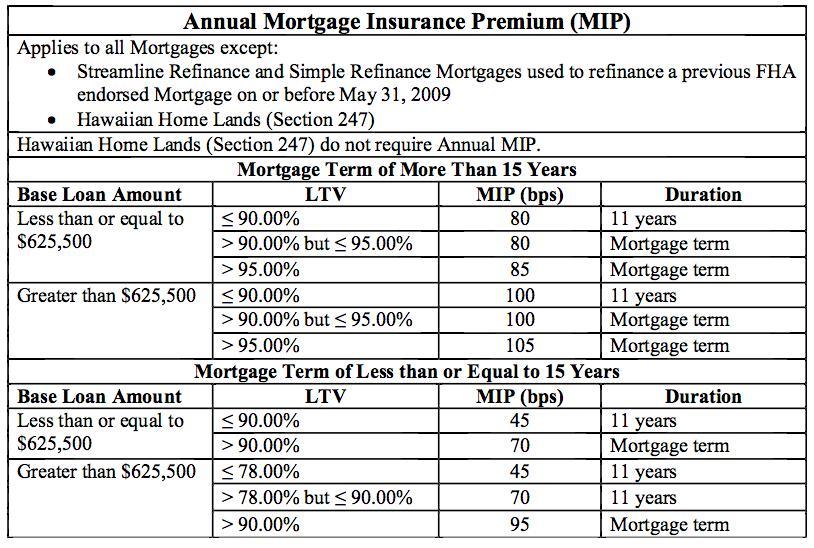

prime mortgage insurance (PMI) is an insurance that mortgage lenders require when borrowers make a down payment of less than 20% of the purchase price of the house.

We are not given any table, so I looked in the internet to find one that can be used as an example:

outstanding principal = $142,000 - 17% = $117,860

- mortgage term equal or less than 15 years

- base loan amount is less than $625,000

- loan to value ratio = 1 - down payment = 83%, which means it is ≤ 90%

- bps = 45

total yearly premium = principal x bps = $117,860 x 0.0045 = $530.47

monthly PMI payment = $530.47 / 12 months = $44.20