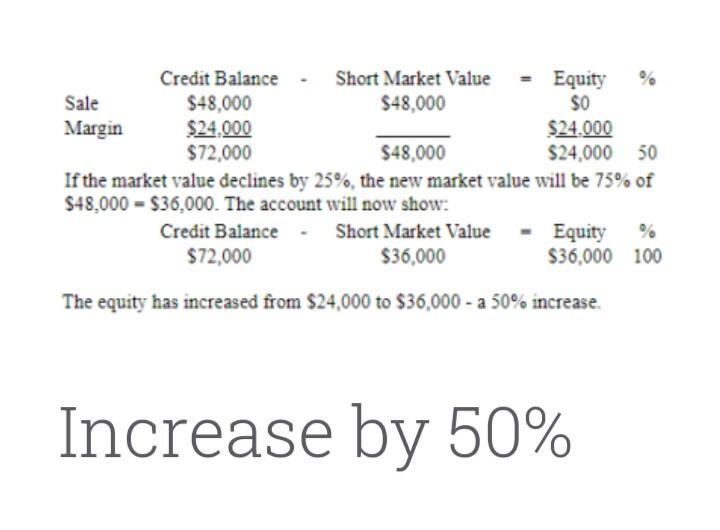

Answer:

It will increase by 50%

Explanation:

Equity is given as: credit - short market value.

Find attached below table of solution

false, higher gear is used for power not for speed

The appropriate response is arousal. One intriguing thing about motivating force methodologies is that motivators exist freely of any need or level of excitement. Excitement and setting best depict Schachter and Singers' hypothesis of feeling.

Answer:

80%

Explanation:

The capacity utilization rate evaluate the proportion of potential economic output that is actually realized.

To solve for theoretical utilization, we use the following formula as given below;

Theoretical Utilization = {p/(ma)}×100

Where we have our variables as,

p=16

m=4

a=5

Imputing variables into the formula we have

Theoretical utilization = {16÷(4×5)}×100

= {16/20}×100

=0.8×100

=80%