Answer:

It will take him 7 years.

Explanation:

Hi! We need to calculate the amount of time that it requires an investment of $34000 to reach $62154 at an interest rate of 9% annually.

By using the formula of Present Value we can isolate n:

The formula is:

PV=Ct/[(1+r)^n]

Ct= cash flow at t time

r= rate

n= period of time

To calculate how many years, we need to isolate n from the PV formula:

n=[ln(Ct/PV)]/ln(1+r)

n=ln(62154 /34000 )/ln(1+0,09)

n=7

Answer:

The amount of the additional projected liability that should be recognized is $28,000

Explanation:

For computing the amount of the additional projected liability, we have to apply the formula which is shown below:

= Tax benefit in 20% - Tax benefit in 40%

= $70,000 - $42,000

= $28,000

The other information which is given in the question is irrelevant. So, it is not been considered in the computation part. Hence, it is ignored.

We took the higher value between $42,000 and $14,000.

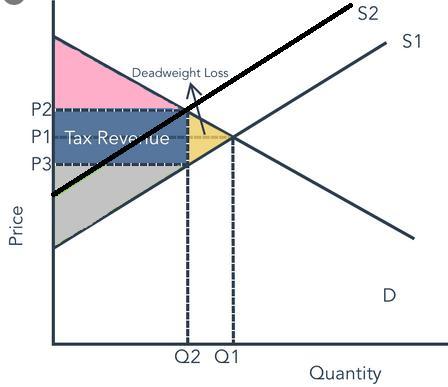

Answer:

deadwweight loss $2,250

Explanation:

The deadweight loss is the area loss between the new consumer and producer surplus after-taxes and the previous consumer and prodcuer surplus after taxes

As this is a straight line then we have the area of a triangle which height is

P2 - P1 in this case the $15 tax levied

and Q2 - Q1 as the high of the triangle in this case 300 units

We now sovle for the area of the triangle:

300 x 15 / 2 = 2,250

The price of the share would be calculated as -

Price of share = Annual constant dividend / Cost of equity

Given, cost of equity = 10.5 %

Annual constant dividend = $ 1.60

Price of share = $ 1.60 ÷ 10.50 %

Price of share = $ 15.238 or $ 15.24

Answer:

Yes

Explanation:

Yes, this concept is an example of supply and demand. When there is a limited supply of a product like the soft drinks in the vending machines then the price would match the number of people that want to buy the product. If in a very hot day more people want to buy a soft drink to cool down then the supply will begin to decrease as more people buy, this will create an increase in price as people would be ok with paying more money in order to be one of the lucky few to get one of the few soft drinks that are left.