Answer:

The budgeted cash payment for September = $37600

Explanation:

Below is the calculation for budgeted cash payments:

The payment for the month August = 40% of 40000 = $16000

The payment for the month September = 60% of 36000 = $21600

In order to find the budgeted cash payment for September, just add the payment for august and September.

The budgeted cash payment = 16000 + 21600

The budgeted cash payment for september = $37600

Answer:

The entry should be:

c. Debit Cash $45,731.25; credit Interest Revenue $731.25; credit Notes Receivable $45,000

Explanation:

Jasper makes a cash loan to Clayborn Co.. This is a Notes Receivable of Jasper.

The amount of the loan is $45,000

Tern of the loan is 90-day and interest rate is 6.5%

The interest amount Jasper receives on maturity date:

$45,000 x 6.5% x 90/360 = $731.25

The entry should be:

Debit Cash $45,731.25

Credit Interest Revenue $731.25

Credit Notes Receivable $45,000

Answer:

a) Get choosy with your fonts and use a font type that matches the company's branding scheme

b) Add a company logo to customer sales forms Use the standard template with no customization

c) Add a splash of color that matches the company's branding scheme

Explanation:

Brand recognition refers to the recognition of the company brand by identifying with the product tag line, logo, advertising, packaging, etc

It could be identified with the help of audio and video clip so that the people could aware of it

Now for building the brand recognition, the following attributes needed

1. Selection of font that matches with the branding

2. Added a logo also the standard template is required

3. Add color splashes

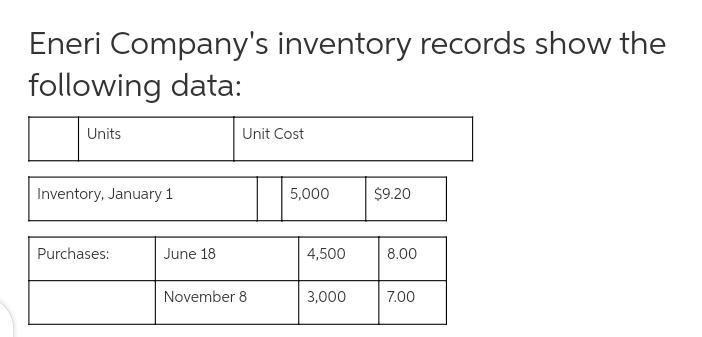

Answer: $29,000

Explanation:

Hello.

Your question was incomplete so I attached a picture showing the missing details.

Cost of Goods sold using First in First Out where the earliest goods are sold first.

Seeing as we have 4,000 units left, that means that none of the stock purchased on the 8th of November have been sold.

1,000 units of the stock purchased on the 18th of June remain.

Cost of Goods sold is therefore,

= 1,000*8 + 3,000 * 7

= $29,000

Cost of goods for Inventory available is $29,000

The option that Mrs. Roberts could consider before selecting a PFFS plan is: A Medicare Advantage Prescription Drug PFFS plan that had both medical benefits and Part D prescription drug coverage.

<h3>What is Medicare?</h3>

Medicare can be defined as a heath coverage that help to cover the medical costs of people under the plan.

Based on the given scenario she should choose a Medicare Advantage Prescription Drug PFFS plan which will includes medical health care benefits as well as a drug prescription coverage.

Therefore she should consider Medicare Advantage Prescription Drug PFFS plan.

Learn more about medicare here:brainly.com/question/1960701

#SPJ1