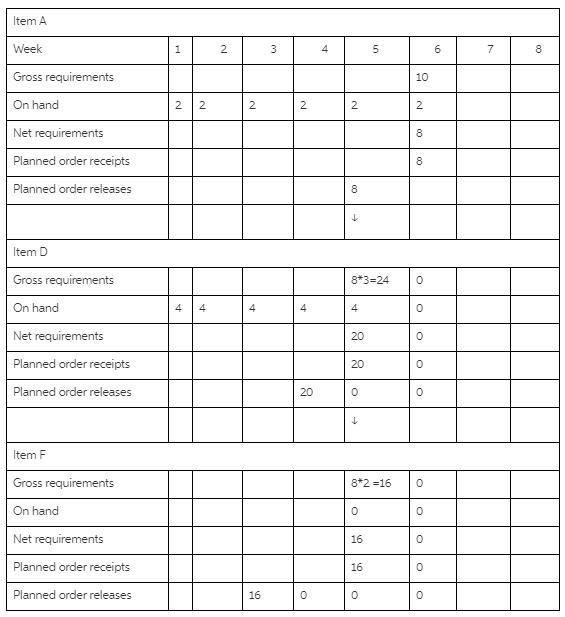

Answer:

Gross requirement for A = 10 units

Inventory on hand for a is 2 units

Net requirement is 10 -2 = 8 units

Therefore Gross requirement of D = 8 * 3 = 24 units (for each A, 3 units of D is required)

and Gross requirement of F = 8 * 2 = 16 units (for each A, 2 units of F is required)

I don’t know the answer but I need points thank you and good luck

Answer:

is personally responsible for all partnership debts

Explanation:

COMPLETE QUESTION

A general partner:

is personally responsible for all partnership debts. has no say over a firm's daily operations. faces double taxation whereas a limited partner does not. has a maximum loss equal to his or her equity investment. receives a salary in lieu of a portion of the profits.

EXPLANATION

A general partner can be regarded as a person that joins with another person or join with more than one other person to form a business. A general partner is responsible for the actions that is been taken in the business, He or she is liable personally for all the debts as well as obligations in the business and can bind the business legally. It should be noted that A general partner is personally responsible for all partnership debts.

Answer:

50,494 units

Explanation:

The sales that must be achieved in order to realize a pretax profit of $167,400 is the total fixed costs plus target pretax profit all divided by contribution per unit

Total fixed costs=fixed factory overhead+fixed marketing costs=$109,500+$111,900=$221,400.00

Contribution per unit= sales price per unit-variable cost per unit

sales price per unit=$968,000/44000=$22

variable cost per unit=($183,500+$241,900+$151,900+$51900)/44,000=$14.30 Contribution per unit=$22-$14.30

=$7.70

target sales units=($221,400+$167,400)/$7.70= 50,494 units

Answer:

an impulse product

Explanation:

When we talk about impulse products we are referring to products that people generally buy on impulse reactions. Generally in a supermarket the aisle just before the cash register is full of candy, chocolates, or other impulse products. Generally impulse products are not expensive so people usually don't think a lot about whether they will buy them or not, they just do it.