Answer:

E. None of the above

Explanation:

because the price level is not known, we can not tell definitely that the output is increased or unemployment is decreased or standard of living is increased

.

Therefore, we cannot conclude on anything.

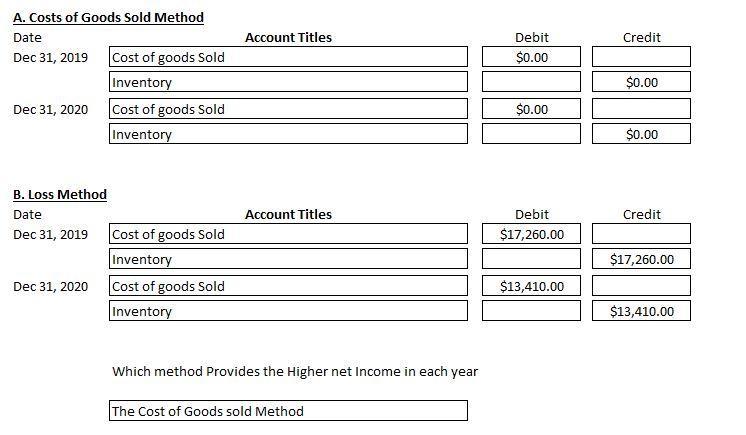

Answer:

Under the cost of good sold method no journal entry will be required. The entries will constitute adjusted along with the sales.

Under the loss method we immediately pass a debit charge to cost of goods sold in the P&L, not awaiting its sales happening.

This makes the net income in that year lower. And makes the costs of goods sold method give a higher net income.

Explanation:

<span>Mort's grandfather had his business strategy, in other words, his own principles, which he put it as ''you pay me when you can, I ain't goin' nowheres''. Mort mentions that cash flow is very important. Indeed, he</span> needs to develop a short-term forecast, which is a prediction of revenue, costs, and expenses for a period of a year or less.

The answer is incident commander

Answer:

The correct answer is: Trial balance.

Explanation:

A Trial Balance is a worksheet listing all of an entity's ledger accounts debit and credit balances. According to accounting theory, the sum of all debits should equal all credits. Because the trial balance is a list of all accounts, it serves as a verification of accuracy.