Answer:

This question is incomplete, the options are missing and the final sentence is written wrong.

The options are the following:

a) People-oriented leadership

b) Managerial leadership

c) Shared leadership

d) Servant leadership

And the correct answer is the option C: Shared leadership

That type of leadership<u> is known as</u> Shared leadership.

Explanation:

To begin with, the <em>"Shared leadership" </em>is the name given to a style of leadership that is used in the companies with the purpose of letting the members of a team to work together as there were no leader at all but instead every member lead each other as the occassions arises and the project goes on. Therefore that this style matches with the description given in where the team members help each other to resolve the situations that evolve as long as the project keeps to continue.

Answer:

Check the safety of the environment and the people

Explanation:

If there are any hazards (electrical, falling, or mechanical) it must be removed ASAP and/or reported. Make sure everyone has their PPE and that it is in good and working condition.

Answer:

The answer is "Risk aversion" ,"Facilitate"

Explanation:

In financial aspects and business, Risk aversion is the conduct of people (particularly customers and speculators), who, when presented to vulnerability, endeavor to bring down that vulnerability. It is the faltering of an individual to consent to a circumstance with an obscure result as opposed to another circumstance with a more unsurprising result yet conceivably lower anticipated result.

For instance, a Risk avert specialist may decide to invest their cash into a ledger with a low yet ensured loan fee, as opposed to into a stock that may have high anticipated returns, yet in addition includes an opportunity of losing esteem.

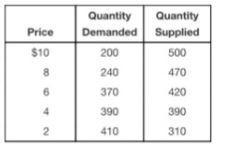

If there was a 100 units decrease at every price level, the new equilibrium price would be<u> $2.00.</u>

<h3>Equilibrium Price </h3>

- Price where quantity demanded is equal to quantity supplied.

<h3>What is the New Equilibrium price?</h3>

Reducing by 100 units, all the quantity demanded units will lead to the following new units:

- $10 - 100

- $8 - 140

- $6 - 270

- $4 - 290

- $2 - 310

We can see that at $2, both the demand and supply are at 310 units which makes this the new equilibrium.

Find out more on the equilibrium price at brainly.com/question/14203212.

Answer:

Walking or using of bicycle

Explanation:

Use of legs are needed in both method of commuting. Leg muscles will be worked up and it also produces sweat that is equivalent to gym exercise