Answer & Explanation:

Most balance sheets are arranged according to this equation:

Assets = Liabilities + Shareholders’ Equity

The equation above includes three broad buckets, or categories, of value which must be accounted for:

1. Assets

An asset is anything a company owns which holds some amount of quantifiable value, meaning that it could be liquidated and turned to cash. They are the goods and resources owned by the company.

Assets can be further broken down into current assets and noncurrent assets.

- Current assets are typically what a company expects to convert into cash within a year’s time, such as cash and cash equivalents, prepaid expenses, inventory, marketable securities, and accounts receivable.

- Noncurrent assets are long-term investments that a company does not expect to convert into cash in the short term, such as land, equipment, patents, trademarks, and intellectual property.

2. Liabilities

A liability is anything a company or organization owes to a debtor. This may refer to payroll expenses, rent and utility payments, debt payments, money owed to suppliers, taxes, or bonds payable.

As with assets, liabilities can be classified as either current liabilities or noncurrent liabilities.

- Current liabilities are typically those due within one year, which may include accounts payable and other accrued expenses.

- Noncurrent liabilities are typically those that a company doesn’t expect to repay within one year. They are usually long-term obligations, such as leases, bonds payable, or loans.

3. Shareholders’ Equity

Shareholders’ equity refers generally to the net worth of a company, and reflects the amount of money that would be left over if all assets were sold and liabilities paid. Shareholders’ equity belongs to the shareholders, whether they be private or public owners.

Just as assets must equal liabilities plus shareholders’ equity, shareholders’ equity can be depicted by this equation:

Shareholders’ Equity = Assets - Liabilities

— Courtesy of Harvard Business School

I hope this helped! :)

Answer:

The correct answer is D. The Tradeoff Theory suggests that a firm should choose a debt level where the tax savings from increasing leverage are just offset by the increased probability of incurring the costs of financial distress.

Explanation:

The trade-off theory of capital structure states that companies choose their leverage ratio to maximize benefits and minimize costs. The classic version of the hypothesis goes back to Kraus and Litzenberg, who observed a balance between the risk of loss of welfare from impending bankruptcy and the tax benefits of outside capital. In the trade-off theory, debt and equity financing are calculated in such a way that the present value of the tax shield is as large as possible and the present value of the costs of “financial distress” is possibly small.

When does accrual basis accounting record a transaction? When under new ownership.

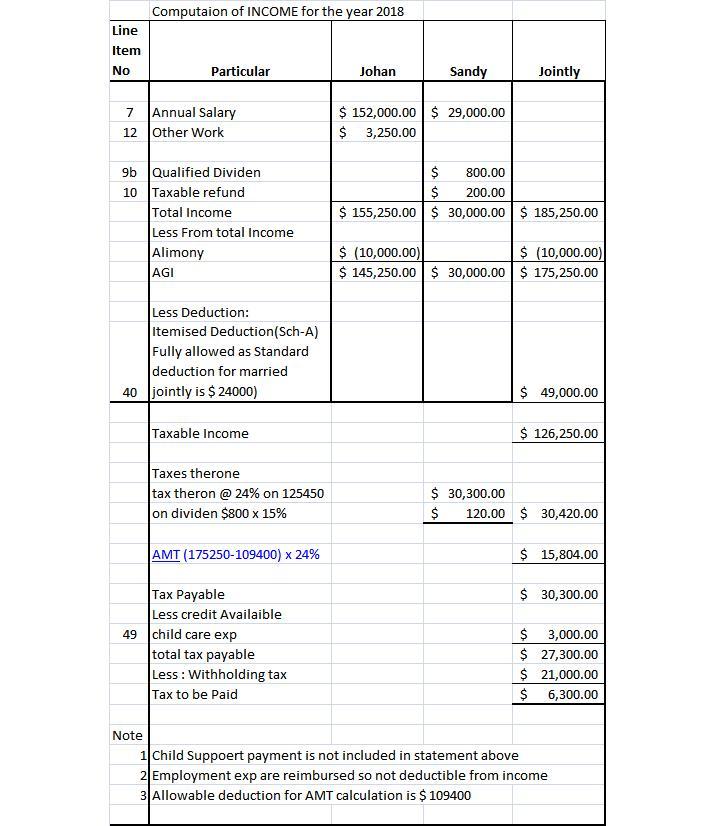

Answer:

Explanation:

The diagram and step by step solution to the answer can be seen in the attached image below

KINDLY NOTE: Self Employment tax (<u><em>which can be said to be a Medicare tax and Social Security paid by self-employed individuals. It is quite similar to the FICA and usually, they are withheld from an employee’s paycheck Medicare taxes and Social Security purposes.)</em></u> is not applicable to both and the AMT is less then the actual normal tax liability so AMT provision also not applicable.