Answer:

Second savings account

Explanation:

Life is full of surprises... repairs or emergency cases this would be helpful to have

I had to look for the options and here is my answer:

Based on the given description above about Doris Lewis who owns Lewis Edibales, Inc., which is a company who makes BBQ sauce and wants to mix goodness that grows in North Carolina, what Lewis is doing is taking marketing actions in order to reach target markets.

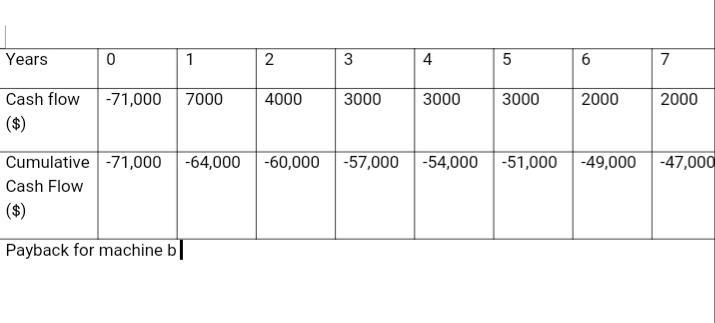

Answer: 0 years

Explanation:

The payback period calculates the amount of time taken to recoup the initial investment made in a project or in the purchase of a machine or building. It calculates how long the cumulative cash flow generated from a project equals the cost of the project.

The payback period for both machines are zero years because the cumulative cash flow is less than the cost of the machine.

For machine A - cumulative cash flow- $-47,000 is less than -$71,000

For machine B - cumulative cash flow, -$7,000 is less than -$52,000

Explanations on how the figures were derived is found in the attached tables.