Answer:

Here is your answer : )

Explanation:

Contractionary fiscal policy means when the government taxes more than it spends.

Expansionary fiscal policy means when the government spends more than it taxes.

Automatic stabilizers means features of the tax and transfer systems that temper the economy when it overheats and stimulate the economy when it slumps without direct intervention by policymakers.

Hope it helps you

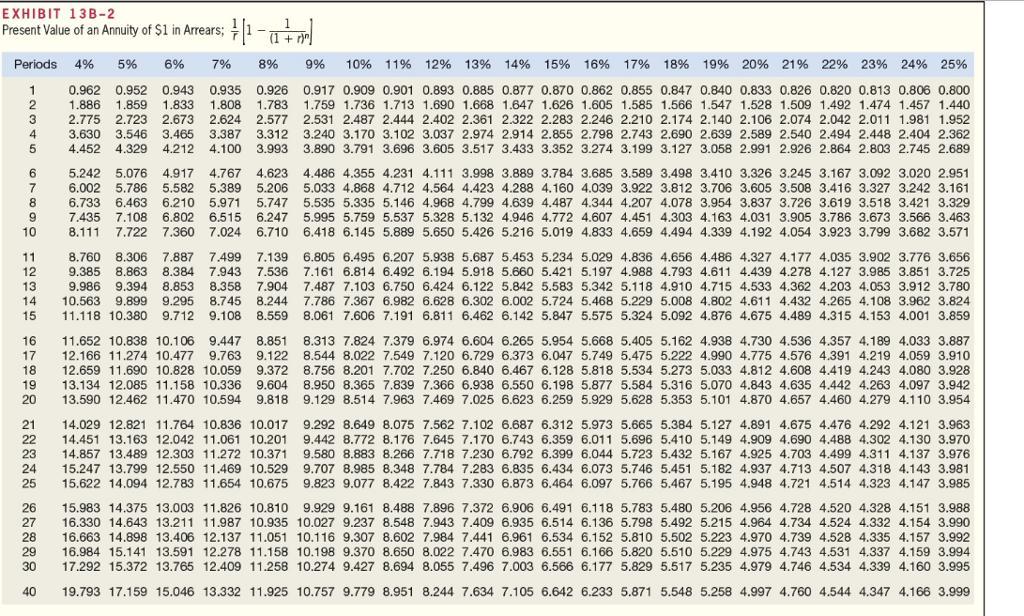

Answer:

12%

Explanation:

initial investment $367,402

net cash flows 1 - 7 = $80,500

the IRR is the interest rate at which NPV = 0

we can calculate it by using Exhibit 13B-2 (present value of annuity in arrears)

$367,402 = $80,500 x present value of 7 year annuity in arrears

- present value of 7 year annuity in arrears at 14% = 4.288

- present value of 7 year annuity in arrears at 12% = 4.564

- present value of 7 year annuity in arrears at 8% = 5.206

with 14% ⇒ $80,500 x 4.288 = $345,184

with 12% ⇒ $80,500 x 4.564 = $367,402 CORRECT ANSWER

with 8% ⇒ $80,500 x 5.206 = $419,083

Answer:

what will happen to the output is that it will decrease due to less consumers and less money to find production, price levels drop(deflation) so will unemployment increase in the shelter on due to no jobs or money to create

Answer:

the question is invalid because there no RHS ana it could not find